You are currently browsing the category archive for the ‘Global Crisis Blog’ category.

2013: Tough Year for Workers, Great Year for HNWI’s

By Shlomo Maital

Illustration by Avi Katz

For most of us, 2013 was yet another hard year. The U.S. and EU economies were either in recession or barely growing. Unemployment remains high; the job market, weak. China faces slowing export growth and a housing bubble.

But it was a super-great year for HNWI’s, the Wall St. euphemism for the rich and super rich (High Net Worth Individuals), who are the focus of a huge and profitable industry known as ‘wealth management’. And wow, is there ever a lot of wealth to manage.

According to the Boston Consulting Group’s Global Wealth 2014 report, global private financial wealth grew by nearly 15 per cent last year and now totals $152 trillion, more than double world Gross Domestic Product. Wealth multiplies with ease, even when the rich do not actively work at it. Microsoft founder Bill Gates, 58, is the world’s wealthiest person, with net worth of $78 b., even though he has spent most of the past few years giving his money away. His Microsoft shares continue to generate more and more billions in wealth for him, even though he resigned as Microsoft Board Chair in February.

Capital has boomed because of urbanization and rising real estate prices, rising share prices, vast amounts of new money printed by central banks everywhere and loaned at low interest, and new capital markets in emerging nations, creating assets where none existed before. Global private wealth boomed last year because investors put money into the stock market and stock markets rose sharply. Wall Street broke all records and closed the year 23.8 per cent higher.

The wealthy have capital and so quickly accumulate more of it; the poor do not. The capital of the rich grows exponentially. The income of the poor stagnates. This is inherently unfair.

But can’t the poor rise to wealth, by hard work and saving?

The American “Horatio Alger” rags-to-riches myth is just that, according to the Equality of Opportunity Project, led by Harvard and Berkeley economists. This study found that an American child born in 1971 to parents in the poorest fifth of the income distribution had an 8.4% chance of making it to the top quintile. For a child born in 1986 the odds were 9%, basically the same. In other words, in the U.S. you have less than a one in 10 chance of rising from poverty to wealth, and it’s been that way for nearly two generations. You need to be fairly rich to go to good schools and to be accepted to good universities. In contrast, in Denmark, the probability of climbing from the bottom quintile to the top one is double that of America. If you want rags to riches, you’d better be born in Scandinavia.

If the democratic system cannot repair itself, because the super-rich control the system through high-paid lobbyists and donations to politicians — what other solution is there? The French Revolution, 1788-1804, used the guillotine; that did not work out too well for anyone and ultimately brought a dictator-emperor named Napoleon, who destroyed Europe.

The rich are different. They have money, and when they invest it, it multiplies rapidly. At 8 per cent compound interest, wealth doubles every nine years. There is nothing wrong with being rich. But when extreme wealth perpetuates itself in the manner now occurring worldwide, poverty perpetuates itself too. Trickle down? It’s a myth, too.

The rich use their wealth to make a whole lot more of it, with ease. That process does not seem to help working people much.

Unless people of good will everywhere, rich, middle-class and poor, get together to resolve this dilemma, society is simply going to fracture, perhaps violently. And that won’t be good for anyone, rich or poor.

Piketty: The #1 Amazon Bestseller Nobody Really Reads

By Shlomo Maital

Can you believe a 696-page boring economics book, Capital in the 21st C., is the #1 Amazon best-seller, and one of Harvard University Press’s (Belknap) all-time best-sellers? And can you also believe very few people have actually ploughed through this tome? And that people constantly mispronounce the author’s name: He is French, and his name is toh-MA pi-ke-TTY, rhymes with bring me TEA!

Bloomberg Business Week has devoted an entire issue to Piketty, his arguments and his criticics, including Chris Giles (Financial Times) and two respected macro-economists, Per Krusell and Tony Smith. (See: http://www.businessweek.com/articles/2014-05-29/pikettys-capital-economists-inequality-ideas-are-all-the-rage ).

As a service to my readers, and to prevent a widespread narcolepsy epidemic (the malady that causes people to fall asleep in daytime), here is a very short summary of the ongoing debate.

What does Piketty claim? Simply – that “Beta” (the ratio of capital to income, for nations) initially fell, but in recent decades has risen. This is because the fraction of income saved (which is what leads to capital accumulation) exceeds the rate of growth of income or GDP.

So what? People who own capital can earn high return on their wealth, averaging 8 %; this doubles their wealth every 9 years. People who spend their income (most of us working people) fall into debt and fail to accumulate wealth.

So what? People with great wealth gain control of the democratic system, to perpetuate their wealth through tax breaks.

The growing concentration of wealth in fewer and fewer hands cannot be corrected by the democratic system (the vast majority, who have no wealth), because the super-rich use their wealth to manipulate the democratic system.

That last paragaph is NOT in Piketty. It comes from an article by John Cassidy, “Is America an Oligarchy?”, The New Yorker, April 18. He quotes two political scientists, Gilens and Page, who claim that: “Our analyses suggest that majorities of the American public actually have little influence over the policies our government adopts”:

Americans do enjoy many features central to democratic governance, such as regular elections, freedom of speech and association, and a widespread (if still contested) franchise. But …in the United States, our findings indicate, the majority does not rule—at least not in the causal sense of actually determining policy outcomes. When a majority of citizens disagrees with economic elites and/or with organized interests, they generally lose. Moreover … even when fairly large majorities of Americans favor policy change, they generally do not get it.

On many issues, say the authors, the rich exercise an effective veto. If they are against something, it is unlikely to happen.

So here is where things stand. Wealth grows faster than income. Wealth concentrates in fewer and fewer hands. Wealth corrupts democracy.

Marx predicted that the concentration of wealth would grow so intolerable, that the proletariat would revolt.

If the democratic system cannot repair itself – what other solution is there?

The World Can Live WITHOUT Perpetual Growth—and It Must

By Shlomo Maital

Today’s Global New York Times (June 5/2014) has a fine column by Eduardo Porter. He refers to Prof. Tim Jackson’s 2009 book, Prosperity Without Growth, and Jackson’s back of the envelope calculation. It shows a bitter truth: The macroeconomic assumption, that continual perpetual growth in GDP per capita is both good and feasible, cannot be sustained. We have to have policies that seek a stable level of per capita GDP, while redistributing wealth and income from rich countries to poor — a very tall order.

Here is the simple arithmetic. Assume that developing nations citizens are entitled to roughly the same level of per capita income as Europe, by 2050 (that’s 36 years away, about a generation and a half!). By then there will be 9 billion people in the world.

- If European incomes grow by 2 per cent annually through 2050, and

- If we want to keep the Earth’s temperature from rising more than 2 degrees C. (3.6 degrees F.) above what it was before the industrial era [in order to prevent violent, unpredictable environmental upheavals], then: the world can emit at most 6 grams of carbon dioxide for each dollar of GDP it produces.

Hmmm… Advanced nations emit 60 times that much, at present! Developing nations emit 90 times that much!

If we want to eradicate poverty (we do) and save our planet (we do), we are going to have to reduce carbon emissions by an order of magnitude. A very tall order, one that will take massive investment of resources, huge creativity, a pro-environment mindset, global cooperation, and a wide variety of new technologies.

President Obama’s new proposal, for limiting carbon emissions, falls far short of what is needed, and even THAT could be sabotaged by Congress (though Obama claims he will implement it as an executive order).

Is no-growth economics possible for rich countries? It is. Look at Japan. Despite Japan’s huge efforts, its per capita GDP has grown very little for two decades. Yet Japan remains a prosperous country, with a high living standard. Is Japan a natural experiment, showing that zero growth is not only possible, but desirable – provided we change our mindset?

I’m afraid that my generation is delivering a ruined planet to the younger generation. They have the right to put us all in jail for this.

Panera – Innovation for People Who Have No Money

By Shlomo Maital

Writing in the Boston Globe, Alyssa Edes tells us about Panera, a French bakery/café that has a new business innovation – give your stuff away, for free, or nearly free.

For example, “when Jonathan Diotalevi walked in to “Panera Cares”, a new Panera branch near Boston’s Government Center, “a smiling employee greeted Diotalevi at the door; he waited in line, ordered a tomato- mozzarella panini, and then asked the clerk, “So, can I, like, just give you two bucks?” Yes, he could. And he did, dropping the money into a nearby donation bin.”

What? No prices? No 30 per cent profit margin? How in the world can you run a business like this? Fox Network will scream that this is a Commie plot to undermine capitalism.

Here is how this branch works. “The restaurant at 3 Center Plaza may have been as busy at lunch time as any of the chains’s other cafes nationwide — more than 1,600 of them — but there’s a reason cochief executive Ron Shaich calls this one “a test of human nature.” The nonprofit outpost of Panera Bread Co. doesn’t have any cash registers, or set prices. Instead, it depends on donations from customers who pay whatever they can afford. The Government Center shop is the fifth of its kind for the St. Louis-based company — the first in this region.”

Note: Some people pay more than the regular price. “I think it’s awesome because it’s obviously beneficial for people who are a little less fortunate,” said customer Yanick Belzile of Lowell. “We can afford to, so we put in a little bit extra. If we can help someone else who can’t pay for a meal, why not?”

“Wayne Gilchrist, who said he lives under a bridge in Cambridge, said he made a modest donation for a coffee and French bread with butter. “I’m homeless,” Gilchrist said. “I got nothing and still gave because I want others to have.” “

About one out of every six Americans, or about 50 million, are “food insecure” or have trouble coming up with enough money to buy food, according to the US Department of Agriculture. “Many of those people work — some of them work two jobs,” said Kate Antonacci, Boston Panera Cares project manager. “Hunger affects people of all types, so it’s not only the destitute we serve. “

When I’m next in America, I plan to eat at Panera. Let’s support capitalists who get it, and who build businesses on the idea that people are basically trustworthy.

This idea could spread. What if businesses charged according to “pay what you can” and “pay what you think is fair”, rather than “pay as much as we can gouge from you, to keep our rich shareholders happy”? Wall St. might never be the same.

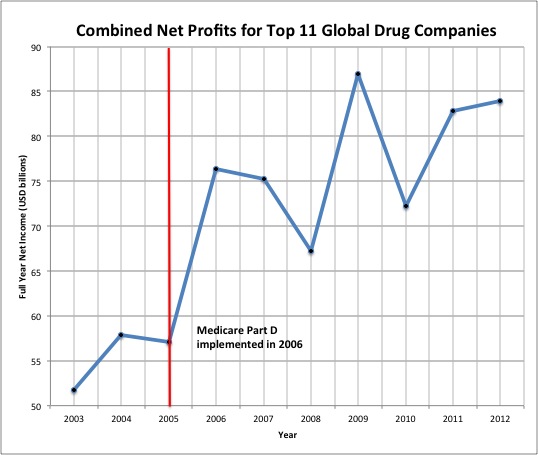

$1.3 b. to develop a new drug? It’s a myth!

By Shlomo Maital

Some numbers, with no basis in fact, become truth simply through repetition. Take, for instance, this one: It costs $1.3 b. to develop a new drug. We all know that, right? That’s why medicine is so expensive.

Wrong. Here is how two eminent doctors (1) debunk that number. And at the same time, prove that “pharmaceutical companies are price-gouging”, with the biggest 11 pharma firms piling up ever-rising net income – nearly $85 b. in 2012.

* Half the $1.3 b. is the opportunity cost of capital invested in developing drugs. An inflated unrealistically high rate of return is used. Right now, the risk-free rate of return on bonds is about 1 per cent. So – knock off fully half of that $1.3 b. We’re at $650 m.

* Taxpayers finance pharma’s research costs, through tax credits and deductions. This brings the $650 m. cost down to $325 m.

* That $1.3 b. is based on the most costly one-fifth of new drugs, NOT the average of all drugs. Correcting this brings the cost down to $230 m.

* A few expensive drugs inflate the average. So it’s best to use the median, not the average. The median: the point at which half of the research projects cost more, and half less. This brings company research costs down to $170 m.

* Pharma inflates the cost of basic research underlying the new drugs. The net median corporate research cost comes down to just $125 m., when the figure is adjusted for more realistic basic research costs. Pharma invests only 1.3 per cent of revenues in basic research; the rest goes to developing new drugs with very little advantage over existing ones, just to inflate profits.

For cancer drugs, most of the cost of clinical trials are paid for by the U.S. National Cancer Institute.

What is worse – big pharma raises the prices on some of their older drugs by 20-25 per cent a year, and in the past decade, they have almost doubled their prices for cancer drugs. This is a ‘market spiral pricing strategy’, at a time when most other new products, like iPhones, fall rapidly in price.

Someone has to blow the whistle on Big Pharma. They are ripping us off, and people are dying because they cannot afford costly medicine. This is inexcusable.

(1) Cancer Rx: The $100,000 Myth. By Donald Light and Hagop Kantarfian. AARP Bulletin: May 2014, p. 22.

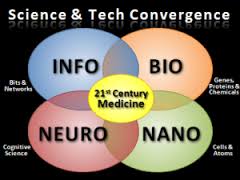

The Three Intersecting Circles of Innovation

By Shlomo Maital

My attention was recently drawn to a three-year-old report, done by MIT scholars, for the health science research community. The report is The Thid Revolution: The Convergence of the Life Sciences, Physical Sciences and Engineering. The authors, which include stellar figures like Profs. Phillip Sharp and Robert Langer, argue that “convergence will be the emerging paradigm for how medical research will be conducted in the future.”

In order for this convergence to happen, they say, we will not “not simply collaboration between disciplines but true disciplinary integration.”

Today, the structure of nearly all the universities in the world is obsolete, ancient, creaky and counterproductive. It is based on faculties, which are silos that work in direct opposition to convergence. The exceptions are research institutes that are cross-disciplinary, specifically nanotechnology. My university has a Nanotechnology Center that draws scholars from many disciplines, and the resulting integration has been tremendously productive. A small example: Prof. Hossam Haick, whose discipline is chemical engineering, but who has harnessed nanotechnology, electronics, chemistry, physics and engineering to produce an ‘electronic nose’, which can sniff cancer molecules, for instance. He recently delivered the first course in Arabic, on Coursera, on nanotechnology.

Structure is not strategy, it is sometimes said. But, sometimes it is. Let’s change the structure of universities. Let’s find a way to restructure them, so that each faculty member has a very clear area of expertise, a clearly-defined discipline, but also has broad knowledge of other fields and above all, works as part of a convergence interdisciplinary team. And for this to work, their offices have to be adjacent…. Despite IT and networking, nothing beats face-to-face conversations over coffee.

Convergence poses a big challenge to those who would innovate. You need to achieve two conflicting goals, both of which are highly challenging.

First, as Nobel Laureate Dan Shechtman repeatedly urges, you must become expert, truly expert, at SOMEthing…. his expertise was in electron microscopy, and it enabled him to overcome fierce opposition to his discoveries, and ultimately win the big prize. You need deep knowledge in at least one field or sub-field.

Second, you need to become curious and learn a great many things about a great many fields, not in depth but sufficient to understand them. You need wide knowledge, surface knowledge, in just about everything. Even if you have team members who have deep knowledge, it still helps a lot to innovate if you have basic understanding of other, distant disciplines.

In future, all the major breakthroughs will occur at the point of convergence among several disciplines. In order for you, innovator, to be there, you need to acquire depth, and breadth.

Good luck!

Ibaka: Mental Toughness Trumps Genius

By Shlomo Maital

Ibaka Blocks Another Shot

Ibaka Blocks Another Shot

Serge Ibaka is a star player for the Oklahoma Thunder, now battling San Antonio Spurs for the Western Conference championship and the right to play Miami (probably) in the NBA finals. Ibaka is from the Republic of Congo, and a citizen of Congo and Spain.

Ibaka is injured. He could barely walk. His team was down 2-0 to San Antonio and on the verge of being eliminated. So Sunday, he decided to play. Oklahoma won 105-92, with Ibaka, a stellar defender who leads the league in blocks, playing a key role. (He is 6’ 10”, 245 lbs., won silver with Spain in Olympic basketball 2012, and gold in the European Championship in 2011.) Oklahoma is a different team when he plays. Kevin Durant and Russell Westbrook score scads of points, but Ibaka is vital for keeping the opponent from scoring.

Why did he play? Ibaka grew up very poor. His family suffered during the Second Congo War; his father was imprisoned. He played basketball on concrete, with worn out shoes or no shoes. He moved to France, then to Spain, playing with second division clubs and working his way up. He was one of 18 or 20 children. His mother died when he was 8. Then civil war broke out in Congo.

Here is what he said, when asked why he played injured. “The military, when they go out there to fight, when they sign up, they sign for evrything. No matter what happened last night, I signed up for this. That’s what I get paid for. When we sign here in the NBA, we sign on everything, man.”

Ibaka was in superb physical condition when he was injured. This is in part why he could come back so quickly. He is known as a rim protector, and is given nicknames like air Congo, Serge Protector and iblocka by his teammates.

Ibaka teaches us that mental toughness, commitment, loyalty, persistence, resilience, and in general character trump genius and innate skills. He has a $12 m. contract with Oklahoma. It hasn’t spoiled him. Because for him, it’s not about the money.

Ibaka reminds me of Fred Smith, founder of Fedex. Smith invested $48 million to launch Fedex. When asked whether he was not fearful of losing the money, he explained that he had served in Vietnam as a Marine, was in life-threatening situations, and “when you can lose your life, losing money has no fear.” Ibaka knew real hardship. Playing hurt, playing through pain, was not even close.

History Repeats Itself: Europe & the Extreme Right

By Shlomo Maital

Nigel Farage, UK

Nigel Farage, UK

History DOES repeat itself.

After WWI (whose centenary, 1914-2014, will soon be observed), the victors (Britain, France) punished the losers (Germany) with outrageous demands for ‘reparations’, at the Treaty of Versailles. J.M. Keynes was there; he warned, in a book The Economic Consequences of the Peace, that the ruinous reparations would lead to a new war. It did. To pay the reparations, Germany simply printed marks. This destroyed the economy through ruinous hyperinflation, and led to the rise of the Nazis and Hitler.

Today, Europe has adopted a misguided policy of austerity, forcing Greece, Spain, Ireland, and to some degree Italy, to adopt stringent spending cuts and tax hikes. True, these countries overspent. But the right way to emerge from excessive public debt is to grow the economy so the debt shrinks and so tax revenues help pay for it. The wrong way is austerity – shrinking government demand, when consumption and investment and exports are all declining. You cannot grow an economy by shrinking demand. Yet many economists support ruinous austerity. Did we forget what Depression did to Germany? Well, it is doing similar bad things to Greece, Spain and other countries.

Now, it is time to pay the Piper. The European Parliament elections have brought a huge victory for parties on the extreme right – Euroskeptics, neo-Nazi, anti-immigrant, and anti-Semitic. It was inevitable. When times are bad, people look to those who have simple remedies – blame the foreigners, the Jewish people, and Brussels.

I’m embarrassed and ashamed to admit I am an economist. Not only do we economists fail to grasp reality, we have also forgotten history, and the warnings of the man who invented macroeconomics, J.M. Keynes.

If the neo-Nazis have risen in Europe, we have nobody to blame but ourselves.

Philippines: Asian’s Next (Surprising) Tiger?

By Shlomo Maital

According to Richard Javad Heydarian, who teaches political science and international relations at the Ateneo De Manila University, “Philippines — along the likes of Mexico – has transformed into one of the most promising emerging markets in the early-21st century.”

This is astonishing, because just six months ago, Philippines was hit by a devastating typhoon. Despite this, it has averaged 7% GDP growth in the past 2 years! This is close to China’s rate.

Notes Heydarian:

“Under the stewardship of the Aquino administration, there has been greater commitment to “good governance”, as exemplified by the ongoing anti-corruption initiatives and investigations. Host to about $300 billion in untapped mineral reserves, Mindanao is poised to benefit from large-scale foreign investments amid an increasingly promising peace process, which has paved the way for the establishment of the Bangsamoro state. No wonder, given our country’s youthful population, natural resources, myriad of tourist attractions, and huge reserve of skilled labor, it has become fashionable these days to talk about the Philippines as the new tiger economy of Asia.”

Emerging market economies in China, Brazil, Russia, and India all have been grappling with inflation, slowing growth, and policy paralysis that undermine decades of robust economic expansion, Heydarian notes.

According to Bloomberg, “Gross domestic product rose 7.2 percent in 2013, the Philippine Statistics Authority said in Manila today, after gaining 6.8 percent in the previous year. That was the fastest two-year pace since 1954-1955.”

A major problem with this stellar growth is that it is not trickling down, and is not benefitting the working classes. This is a common phenomenon in emerging market countries. Heydarian writes, “Poverty and unemployment figures have hardly changed, while inequality is intensifying. Few major businesses swallow newly-generated growth, while the majority of the population is yet to benefit from the recent economic boom.”

Can Philippines sustain its growth? Many Filipinos work abroad; their remittances fuel high domestic consumption. There has been a real estate boom as well, and a boom in services. A fifth of the Philippine government’s national budget goes to debt service, leaving too little for health and education.

Philippines can leverage a pro-China strategy, pulling in investment that may leave Vietnam and Indonesia, in the wake of anti-China sentiment. Philippines too has maritime disputes with China, but seems to have handled them wisely. If other southeast Asia nations let the left-brain emotions govern their right-brain logic, Philippines stands to gain.

Could we perhaps hope that Philippines will finally build a world-class airport? Manila has been voted recently “the world’s worst airport”. Filipinos and travelers deserve better.

2013: Tough Year for Workers, Great Year for Billionaires

By Shlomo Maital

Last year, 2013, was not too great for the working people of the world. Unemployment remains high in most countries, especially the U.S. and Europe, and is highest among the youth. Economic growth is stagnant in the U.S. and EU.

But guess what. It was a GREAT great year for billionaires. According to Forbes magazine, which carefully documents (and generally worships) the super-rich, there are 1,645 dollar billionaires in the world — 268 more than the previous year, an increase of 17 per cent. The world’s billionaires owned wealth totaling $6.4 trillion, up from $5.4 trillion a year ago, a 19 per cent rise!

The total wealth held by only 1,645 persons, $6.4 trillion, is bigger than the GDP of any country, except the U.S. and China.

Who tops the list? Well, it’s Bill Gates again, with personal wealth of $76 b. (mainly through Microsoft stock). And here’s the point. Bill Gates isn’t TRYING to make money any more. In fact, he’s working very hard, with his wife Melinda, to GIVE AWAY his money effectively and impactfully.

So, to those, like Financial Times’ Chris Giles, who want to refute Thomas Piketty’s findings — answer this. How can you deny, that great wealth perpetuates itself, and grows itself, at huge rates of increase, even when the owners of that wealth aren’t even trying to add to it?

America has the most billionaires, 492 of them; China is a surprising second, with 152, and Russia, third, with 111. America has 1.55 billionaires per million people; China has 0.11 billionaires per million; and Russia has 0.77 billionaires per million. Most of Russia’s billionaires stole the assets that rightly belong to the Russian people.

So – dear Bill Gates: It certainly is true that if you’re born poor, it’s not your mistake, or your fault. And the way the world is, chances are very high, you are born poor. But Bill, if you die poor, which is what happens to most poor people, it definitely DEFINITELY is not your mistake. Because the world is enormously tilted toward those who already HAVE money. Fact. And your wealth is proof.

If you die poor, it is because those who control $6.4 trillion of the world’s wealth, which they accumulated on the backs of hard-working people, are using it to generate more and more and more wealth, and hang onto it, instead of using it to help others without money get more of it. Bill Gates and Warren Buffett are exceptions that prove the rule.

And Chris Giles? What else would you expect from the Financial Times?