You are currently browsing the tag archive for the ‘inflation’ tag.

Trumponomics

By Shlomo Maital

(from The Economist)

“Trumponomics” is the economic theory that drives President Donald Trump’s planned economic policies. It includes low interest rates; tariffs on China, Mexico and Canada, and anyone else that sells more to the US than it buys; expelling immigrant workers; slashing taxes; removing renewable energy subsidies.

What can we expect? Here is Olivier Blanchard’s ‘take’. He is an MIT economics professor, former chief economist of the IMF.

“….perhaps the most crucial issue is what the Fed will do. If it sticks to its mandate, it will stand in the way of some of Trump’s hopes from the use of tariffs, deportation, and tax cuts. It will have to limit economic overheating, increase rates, and cause the dollar to appreciate. The big question is thus whether Trump can force the Fed to abandon its mandate and maintain low rates in the face of higher inflation.”

To explain: The US already has a huge federal budget deficit, some 7% of GDP. US public debt exceeds its annual GDP. Trumponomics tax cuts and gifts to the wealthy will further hamper revenues and increase the deficit. Tariffs will make goods and services more expensive for consumers (no, people, it is not the Chinese or Canadians who will pay the tariffs, it is us). The result will be more inflation, rather than, as promised, less.

Enter the Fed: Higher inflation brings tighter interest rates. Trumponomics is in love with low interest rates. Result: A cataclysmic conflict with Fed Chair Jerome Powell, who remains in his post until 2026. At that time, Trump may try to appoint a non-mainstream new Fed Chair, who will maintain low rates in the face of inflation – leading to more inflation.

The US has been successful since 1776, mostly, because its Judiciary (Supreme Court) and its money people (Federal Reserve) have been constitutionally isolated from political influence, in general. The judiciary now has a Trump majority. When the Fed too falls into Trumponomics – yikes. Risk premiums on US bonds rise, as capital markets start to wonder whether the US may, like Nicaragua or South Africa, fall into fiscal decay.

Here is Blanchard’s conclusion: “Fed Chair Jay Powell has made clear he remains committed to the mandate and to staying at the Fed as chair until his term as chair expires in May 2026 (his term as board member ends in 2028). Current Fed board members are unlikely to follow a different line. But one board position opens in January 2026, and Trump could seek to name a more docile board member to the seat. If this is the case, and the board goes along (which is unlikely), the result will be low rates, overheating, and higher inflation. Given the unpopularity of high inflation, not to mention the reaction of financial markets to the loss of Fed independence, this prospect may be enough to make Trump hesitate to pursue this option.”

Stay tuned! We are headed for interesting times.

If the US Economy is So Good – Why Is It Perceived as Bad?

By Shlomo Maital

Many experts – and Democrat strategists – fretted, worried, puzzled, pontificated and blustered over why the US economy did so well, by the numbers, and was perceived as so bad by working people.

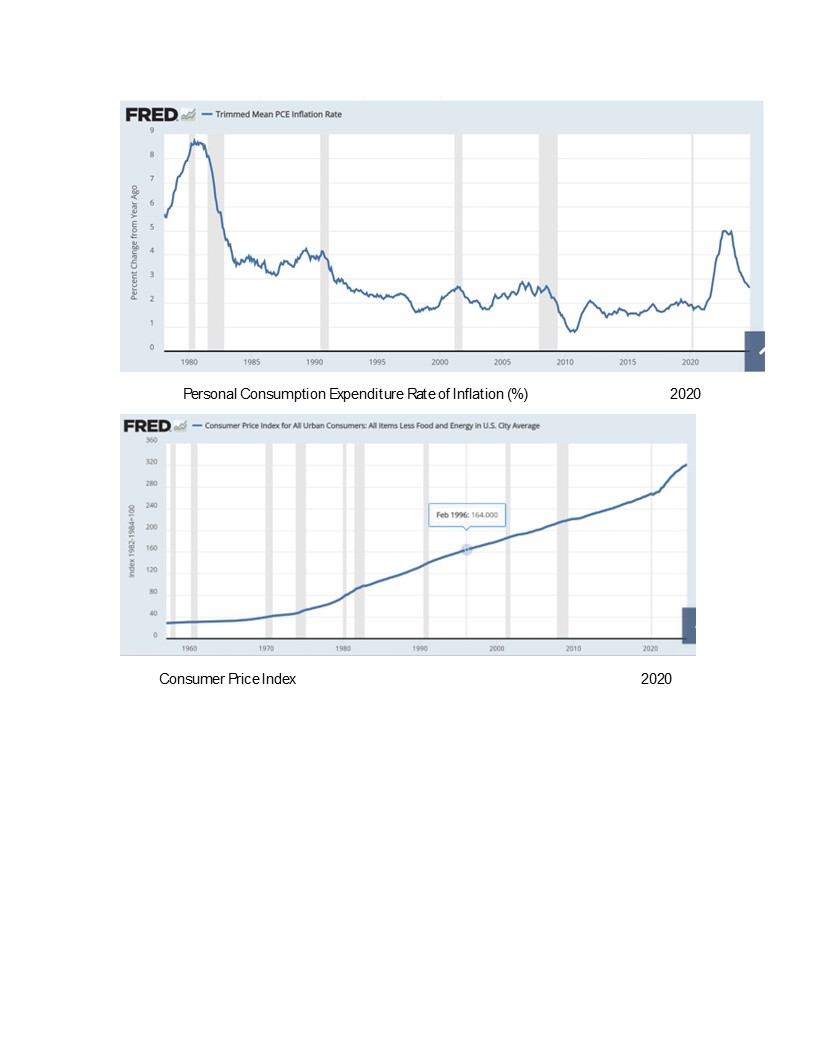

The above two graphs, thanks to the St. Louis Fed’s superb software “FRED”, provides an explanation.

In 2020 inflation (measured by the year to year percentage change in the personal consumption expenditure price index, which measures the price of what people buy) peaked at over 4% — and then fell sharply to around 2 per cent, leading the Fed to slash interest rates. See the top graph.

Good news, right?

In October 2024, just before the US Presidential election, the consumer price index was 321.7, up from April 2020’s level of 265.7. That is an increase of 21.7%. That means – what people bought just before the election was 21.7% more expensive than in April 2020, just before Biden won the election. During that time, the wages of low-income working people did not come close to rising by 21.7%. That means, a lot of people were struggling in 2024 to buy what they bought relatively easily in 2020. See the bottom graph.

The difference is simply this: Some measure inflation by the rate of change But ordinary people measure it by what they can buy at the supermarket. Good work for bringing down the rate of inflation! But – did you fix the damage the inflation did before you got it under control? Raised the national minimum wage to $15? No? Then – you will lose the election.

Paul Volcker, 1927-2019: How He Saved the World from Inflation

By Shlomo Maital

Paul Volcker 1927-2019

Paul Volcker has passed away; he was 92. Volcker served as Chair of the Federal Reserve Bank, appointed by Jimmy Carter in 1979.

Volcker was a giant, physically, standing 6 ft. 7 inches tall – but also a giant in wisdom and courage. The US was afflicted by double digit inflation, from 1979 to 1981, driven by cost-push price rises and soaring oil prices. Volcker quickly understood the threat. With the dollar serving as the world’s major, perhaps only, globally-accepted currency, US inflation threatened not only the US but also the global trading system, then struggling from recessions in 1973 and again in 1978/9.

Volcker acted with what then seemed like outrageous boldness. He raised Fed interest rates to 21%. This was unheard of. I can only imagine what today’s President, Donald J. Trump, would have said, had he (heaven forbid) have been president at that time. Trump wants zero interest rates, no matter what the economy needs, and has hassled current Fed Chair Jerome Powell over his unwillingness to promote cheap credit at all cost and at all times.

Volcker’s move put a halt to the inflation, stopping it in its tracks, but also ground the economy to a halt, causing a recession, or what came to be known as stagflation. Partly as a result Jimmy Carter became a one-term President, defeated in November 1980 by Ronald Reagan. It was ironic that Carter lost partly because of a very wise and strong appointment that he made, to the Fed.

We must remember Volcker and the strong independence of the Federal Reserve system that prevailed, until now. No President has dared messing with the Fed’s independence, until now. Research shows that nations with strong independent central banks fare far better than those where governments make their central banks into private money-printers. Trump endangers today’s Fed, and as a result, endangers the world. We should remember Volcker fondly, and recall the lesson he taught us.

Goal-Driven Innovation: the Case of U.S. Health Care

By Shlomo Maital

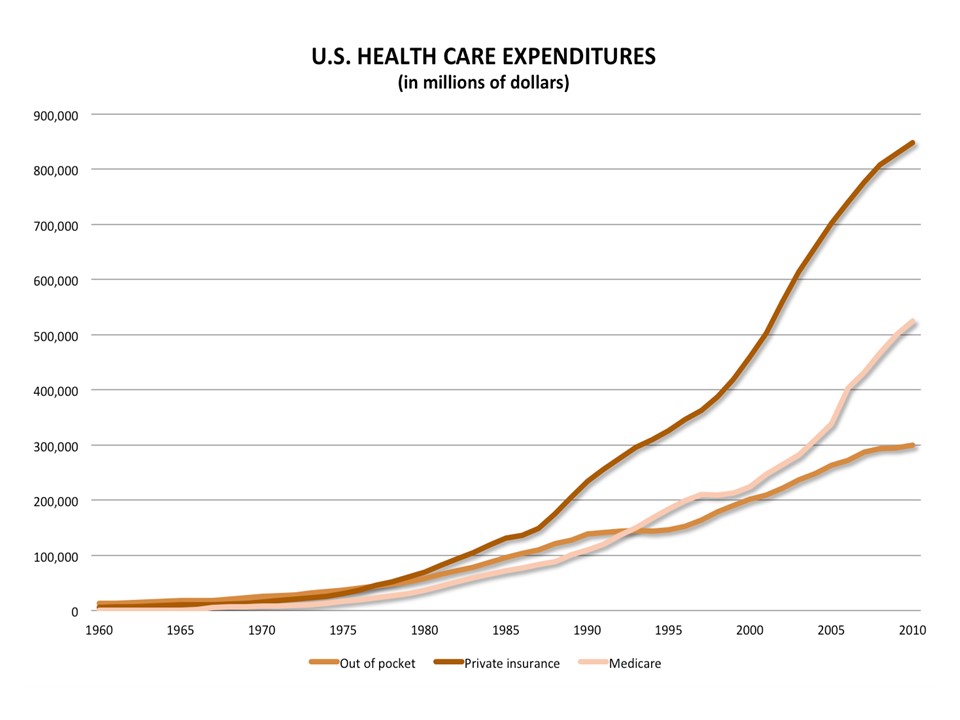

U.S. health care expenditures ($billion)

The U.S. spends 18 per cent of its GDP on healthcare. Much of the recent rise in healthcare spending has been driven by higher prices and costs.

In any industry faced with rising costs, innovation must play a role. Harness creativity, ideas, new thinking, to get costs under control. Yet in healthcare the opposite has happened. More and more innovation has created amazing medical technologies that costs astronomical sums – devices, drugs, etc. Innovation became part of the problem, rather than the solution — it’s great to know that you can save lives, but how many people can afford to have their life saved, at those prices?

Writing in today’s Global New York Times, David Brooks notes that healthcare inflation seems to be under control, and partly, as a result of cost-saving innovation:

“ …Recently health care inflation has been at historic lows. As Jason Furman, the chairman of President Obama’s Council of Economic Advisers, put it in a speech to the Hamilton Project last month, “Health care prices have grown at an annual rate of 1.6 percent since the Affordable Care Act was enacted in March 2010, the slowest rate for such a period in five decades, and those prices have grown at an even slower 1.1 percent rate over the 12 months ending in August 2015.”

There is naturally some controversy over why precisely health care prices have stabilized. But here is one theory:

Jonathan Rauch, in a report for the Brookings Institution, argues that the health care market is more open to normal business model innovation than ever before. The quality of health care data and analytics is improving exponentially. Pressures to reduce costs are ratcheting up. Profitable niches are growing for efficiency improving products. In the past, most innovation involved improving quality of care at high cost. Rauch described many entrepreneurs who are providing innovations that maintain current quality of care but at lower cost. We seem to be making at least some incremental progress toward a structural reduction in health care inflation.

Innovation indeed is regarded as a panacea, when the world faces severe problems, as with healthcare provision, and increasingly severe budget and resource constraints.

But the innovation effort has to be focused, with a goal. If health care inflation is the problem, direct your innovation efforts toward controlling and reducing costs, rather than ever-more-expensive gadgets and drugs that make the problem worse.

Like all human activity, innovation needs a clearly defined goal – a precise question to which it is directed. For America, the question should probably be: how can we use our creative thinking to keep healthcare prices stable? So far, it seems to be working.

When Is Good News Bad News? When It’s the Stock Market

By Shlomo Maital

Love that stock market! It goes up on bad news, down on good news. Can we understand why?

I belong to a panel of the German Ifo Institute, that quarterly surveys experts around the world to assess the global economic situation. The latest report? “world economic climate deteriorates, economic expectations less positive, inflation expectations remain low, US dollar expected to rise (it has), interest rates look set to remain stable (maybe not).”.

The U.S. stock market has risen sharply in the past year. But it recently declined. Why? Good news on the American economy – U.S. job creation and GDP growth are stronger than expected.

Run that by me again? How can good news be bad news for the stock market?

It’s simple. Wall St. is incurably addicted to cheap money and low interest rates, and plentiful credit. When the economy gets stronger, it increases the likelihood that Janet Yallen and the Fed will raise interest rates, ending the era of cheap money, and denying Wall St. from its daily/weekly fix of low-interest cash, used to speculate and earn billions. So the stock market drops, because good news for the economy is bad news for Wall St.

Does this show a sharp conflict of interest between the general population and the moneybags who run Wall St.?