Costs and Benefits: A Disastrous Asymmetry

By Shlomo Maital

An economist, it is said (and I am one), is one who knows the cost of everything – and the value of nothing. There is much truth to this saying.

Costs are pretty easy to measure. You add up the numbers in financial statements or government budgets.

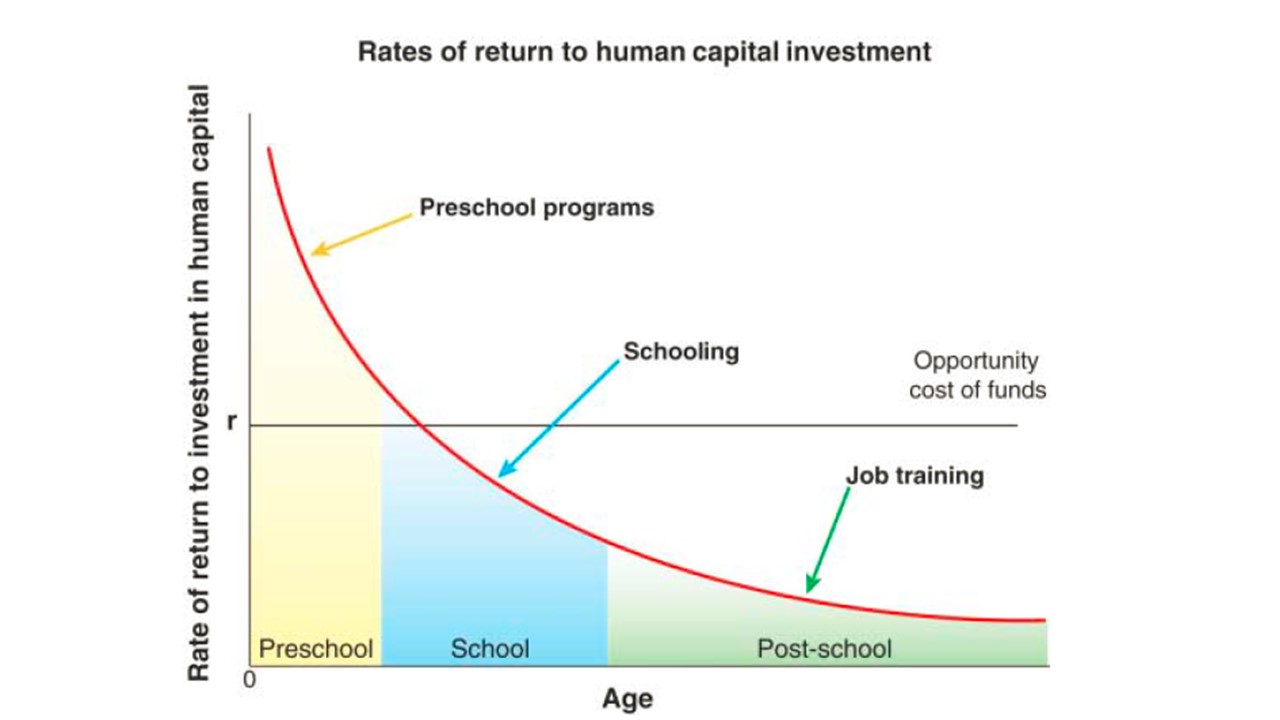

But benefits? Fruits? Now that’s another story. Because many social benefits are long-term and indirect. There is a famous study by Nobel Laureate James Heckman of the pre-school program known as Head Start, where funding has been drastically cut.

Heckman writes in SCIENCE, 2006: “at current levels of funding, we overinvest in most schooling programs, and underinvest in pre-school programs for disadvantaged children”. The diagram above shows this. Pre-school investment has a social return above the opportunity cost of the money. Other programs for older children fall short. Why?

Because the benefits we reap from pre-school (mainly the Head Start program) are long-term, accruing in adulthood, hard to measure, hard to track – and beyond the myopic vision of political leaders, especially Republicans.

Here is another example of this dreadful cost-benefit asymmetry:[1]

The study shows that, under plausible scenarios, the societal cost savings generated from fewer evictions and foreclosures could equal half of the cost of subsidizing coverage for the near-poor.

Low-income people who gain health insurance are much more likely to make their rent and mortgage payments, according to a new Washington University study of families living near the poverty line. Lower delinquencies mean fewer foreclosures and evictions. Researchers found that near-poor households that enroll in subsidized Marketplace insurance are 41 percentage points less likely to become delinquent on home payments compared to similar uninsured households. As a likely consequence, the rate of home delinquency for households without access to employer insurance fell by 31 percent at the income eligibility threshold to receive Marketplace subsidies during the 2015-2016 period. The study, performed at the Center for Social Development at the Brown School of Social Work and the Olin Business School, is one of the first to show the effect of the Affordable Care Act on family finances and the first to show the financial impact of the Marketplace component of the program, in particular. “Our results indicate that lower home payment delinquency may be an important benefit from subsidized Marketplace insurance,” the authors write.

“The spin-off benefits to the community may offset a substantial share of the cost of the subsidy program,” said lead researcher Emily Gallagher. “Not only do the banks and landlords benefit, but the entire community gains through lower rates of homelessness and abandoned property. There are fewer vacant homes dragging down housing values in the neighborhood.”

Republicans in the Senate are about to kill Obamacare (the Affordable Health Care Act) and deprive 23 million people of health insurance. The main motive is cost saving. The result will be to again increase defaults on home mortgage payments, eviction, decaying neighborhoods and vast human suffering. And all, because of cost-benefit asymmetry, and blindness to long-term indirect social benefits.

By the way – many Senate Republicans have not yet seen the actual proposed legislative bill. Senate Majority Leader Mitch McConnell has kept it a state secret. Thus does calumny thrive in the dark, like mold.

Leave a comment

Comments feed for this article