You are currently browsing the tag archive for the ‘China’ tag.

Chinese Innovation: On the Rise

By Shlomo Maital

An insightful new report by McKinsey Global “China’s Innovation Imperative” sheds important light on China’s massive effort to become more innovative.

Here are some of the report’s key insights:

* “to realize consensus growth forecasts—5.5 to 6.5 percent a year—during the coming decade, China must generate two to three percentage points of annual GDP growth through innovation”. In other words up to half of China’s GDP growth must come from innovation. This is no easy task.

* “…about 40 percent of the increase in total factor productivity could come from innovations in higher-level manufacturing and services enabled by the Internet. Other innovations could come from catch-up activities that bring Chinese enterprises up to global best practices as well as breakthroughs yet to emerge. China will have evolved from an “innovation sponge,” absorbing and adapting existing technology and knowledge from around the world, into a global innovation leader.”

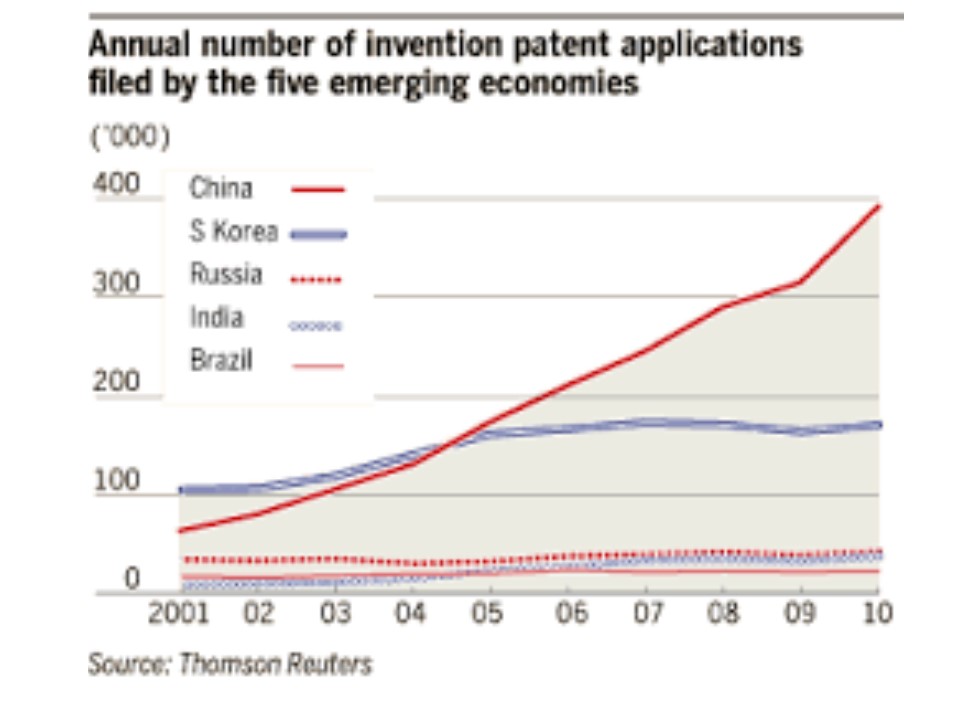

* “China has become a strong innovator in areas such as consumer electronics and construction equipment. Yet in others—creating new drugs or designing automobile engines, for example—the country still isn’t globally competitive. That’s true even though every year it spends more than $200 billion on research (second only to the United States), turns out close to 30,000 PhDs in science and engineering, and leads the world in patent applications (more than 820,000 in 2013).”

* “…we identified four innovation archetypes: customer focused, efficiency driven, engineering based, and science based. We then compared the actual global revenues of individual industries with what we would expect them to generate given China’s share of global GDP (12 percent in 2013). As the exhibit shows, Chinese companies that rely on customer-focused and efficiency-driven innovation—in industries such as household appliances, Internet software and services, solar panels, and construction machinery—perform relatively well.”

In general, China has strengths in process innovation, as it proves each time it takes production blueprints from a foreign firm and quickly produces the product. China also appears strong in incremental innovation. Perhaps a new focus should be placed on radical innovation – game changing new ways to create value and to do business.

The mantra of China’s 13th 5-year-plan is “China dreams”. Dream big, China.

Wrong-Way RMB?

By Shlomo Maital

Financial Times reports that “China devalued the yuan by the most in two decades, a move that rippled through global markets as policy makers stepped up efforts to support exporters and boost the role of market pricing in Asia’s largest economy. The central bank cut its daily reference rate by 1.9 percent, triggering the yuan’s biggest one-day drop since China ended a dual-currency system in January 1994. The People’s Bank of China called the change a one-time adjustment and said its fixing will become more aligned with supply and demand.” The renminbi is seriously undervalued; its purchasing power is about 4 RMB per dollar, not 6. So why devalue it, send it in the other direction?

What is going on?

Well, depends who you believe. Financial Times’ ‘take’ is that China is starting a currency war, a la 1930’s, with countries competitively devaluing their currency to gain export markets and stimulate their economy, while exporting unemployment. The small 2 % devaluation shows China’s leadership is “desperate”:

According to conventional wisdom, wars are easy to start and difficult to end. Similarly Beijing’s devaluation, the biggest one-day currency move since 1993, represents the latest skirmish in an emerging battle which, analysts warn, may be hard to reverse. The move marks a shift in China’s historical policy during times of economic stress. In the late 1990s, the country was widely credited with containing the destruction from the Asian financial crisis because it held fast to the renminbi exchange rate in the midst of competitive devaluations throughout the region. In the global financial crisis of 2008, Beijing also refused to devalue even as its exports, a key driver of the economy, evaporated overnight. But now, in the midst of a pronounced and persistent Chinese economic slowdown and continued appreciation pressure resulting from the renminbi’s “dirty peg” to the soaring US dollar, China’s leaders have decided to take the plunge. “This shows how desperate the government is over the state of the economy,” said Fraser Howie, a China analyst and co-author of Red Capitalism. “If they were trying, as the central bank said it was, to bring the exchange rate back into line with market expectations then they have failed miserably as the market is now just expecting further devaluation.”

But here is Neil Irwin’s ‘take’, in The New York Times: China is seeking twin goals, keeping the flagging economy going and establishing the RMB as a global currency, by allowing market forces to work, rather than pegging the RMB artificially to a soaring dollar.

And my own view: With the dollar losing its pre-eminence as a world currency, largely because the Fed has printed far too many of them, for domestic policy purposes, the world does need a strong well-managed global currency. It could be the RMB?

Who is right? Well, dear reader, in this, as in other issues, you’ll have to think for yourself. The main thing is, be sure you are fully aware of the real issues the world faces, and not some of the puff pieces that fill our newspapers and news websites. China, and everything that goes on there, is one of those key issues.

The Purpose of Life: Ask Walt Disney?

By Shlomo Maital

Last month, I taught a one-week course on entrepreneurship and creativity to 43 dynamic Chinese students, mainly undergraduates studying at Shantou University, Shantou (Guangdong). The course was in English; the students worked on business plans in teams, and made elevator-speech presentations (in English), prepared 2-minute videos, and wrote business plans (in English). (The photo shows a Play-Do, or plasticene, model of one of the team’s ideas, for a novel restaurant – they stayed up all night to create it!).

I just received an email from one of my students. I pasted it below, without correcting the syntax… (Shantou University has a phenomenal English Learning Center, that provides each student with a tailored personal program for learning to read write and speak English)….

I want to ask you a personal question, this question had confuse me for a very long time, the question is that “what do we live for?”, what’s the point of live? create value? make money? love? i not sure. now i just in my 20s age, i always feel there’s no a direction in my life, i’m not sure what is going on in my rest of life. but you have a lot of experience about life, you have make a lot of achievements in your life, so want to ask your answer about the question, i hope you can give me some suggestion.

Dear readers: How would YOU answer my wonderful student?

My own answer was rather woeful – but, here it is. Congratulations for just asking the question. Most of us ask it, at the end of our lives, when it is nearly too late to actually change anything. I think the purpose of life is best defined by Walt Disney. He set the mantra for Disneyland (later, Disney World): “Make people happy”. Create value. Use your brains, your courage, your intellect, and above all, your CREATIVITY – to create value, by widening people’s range of choices, and thus, making them happy, or at least happier. When you make other people happy (those around you, family, children, spouses, relatives, friends, total strangers), you will make yourself happy as well. If you only try to make yourself happy, in the end, you will be very alone.

What I Learned in China

By Shlomo Maital

I try to write a blog almost every day – knowing this keeps me ever alert for new ideas to share. In this sense, blogs are as much for the benefit of the writer as for the reader.

I’ve been in Shantou China, for a week, teaching entrepreneurship to 43 eager young undergraduate business majors at Shantou University. Shantou is in the northern part of Guangdong Province, north of the provincial capital Guangzhou, close to the coast, and two hours by fast train from Shenzhen, which is opposite Hong Kong, on the mainland. My university, Technion, has a joint venture with Shantou Univ., to establish GTIIT – Guangdong Technion Israel Institute of Technology, now headed by Technion Nobel Laureate Dan Shechtman. The initiative arose from a generous grant by Li Ka Shing and his Third Son Foundation; Li Ka Shing, a Hong Kong billionaire, was born in Shantou and his foundation is active in supporting the city and its university. His investment company has invested profitably in Israeli startups.

Supposedly you cannot teach entrepreneurship to undergraduates because “they are too young and lack experience”. But Babson College does it highly successfully, using the method developed by my late friend Ted Grossman, an action learning approach in which teams of students form a real company, make a real product and learn the tools of business through running their company, under the guidance of mentors like Ted (who first launched a successful software company before joining Babson).

I use the same method in Shantou. And in one intensive week, the young students do amazing work; some of their ideas become reality, though not all. The photograph shows last year’s class.

Wages in China have risen dramatically, from about $100 a month in 2000 to $650 today (this is still only one-fourth the average wage in America, and Chinese productivity is in many cases even higher). But Philippines, for instance, has average wages of only one-sixth that of China. So China in principle should be losing its manufacturing to low-wage countries like Vietnam, Indonesia, and Philippines. And indeed it is, with shoes and textiles, low value added products, moving to those countries.

But China is keeping its high value-added jobs and enhancing them. How? China is the world’s biggest market for production robots, buying 20 per cent of worldwide production. Labor productivity rose by 11 percent yearly (!) on average during 2007-12 (it barely budged in the West). China uses its network of highly efficient suppliers to keep factories in China. China has become the hub of a complex ecosystem, in which Asian countries specialize, make components and ship them to other Asian countries. Asia now accounts for nearly half of all world manufacturing output, compared with 27 percent (about one quarter) in 1990.

Bottom line: China’s strategy is: Made in China 2025 (its official name) – boost productivity to keep competitive. If wages rise by 12 percent year but productivity does too…the cost advantage stays. But at the same time: Created in China. China is working to invent more of the products it makes. Like Xiaomi, the innovative smartphone company. And this is where I come in… teaching innovation to the young undergrads at Shantou University, not even a tiny drop-in-the-bucket in huge China, but – China is all about scale, and good ideas spread with lightning rapidity.

I truly love my annual one-week courses in Shantou; the students are fiercely eager to learn and highly creative once their creativity machines are turned on. These young people are literally eating our (Western nations’) lunch. If we don’t wake up, China’s living standards will continue to grow by 11 or 12 per cent a year, the rate of growth of productivity, and our living standards will simply stagnate (the rate of growth of OUR productivity). We need to save more, invest more, build better infrastructure, educate our young people better, and become more productive. This is what I learned in my classroom from 43 eager young Chinese business-major undergraduates.

China: Big Nation, Big Worries

By Shlomo Maital

A new survey shows that half of Americans believe the recession is still alive and well, despite the booming stock market. And close analysis shows that the world’s second biggest economy, China, also has big worries. So when the world’s two largest economies are struggling, global managers need to be on their toes, to daily track events and manage risk.

My friend Clyde Prestowitz, formerly President Reagan’s trade advisor and now head of Economic Strategy, has provided us with some quality insights into China’s current predicament. “This is the start of a new ball game with China,” Clyde warns. Here is a summary:

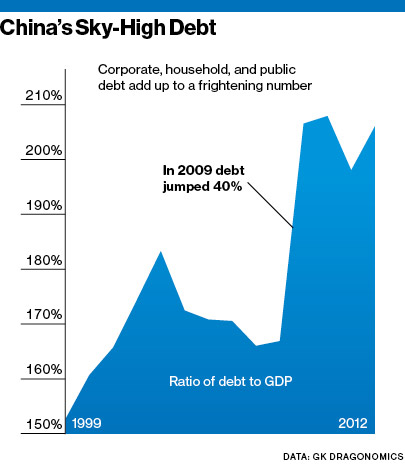

- Xi Jinping’s two major goals are: 1)Restore the power of the center and ensure the sustainability of the Party’s rule. 2) Restore China to its historical position of prominence of the world stage. This marks a departure from the line of Deng Xiaoping who urged : “observe calmly, secure our position, cope with affairs calmly, hide our capacities, bide our time, maintain a low profile, and never claim leadership.” ● Two schools of thought now contend in Beijing – one advocating the low profile approach, the other saying that this low profile has encouraged Japan and other Asian countries to push their claims in the North and South China Sea, and arguing that it is now time to show a more assertive posture. ● Xi seems clearly to be leaning toward this latter approach: What he is now basically saying to the US is rather something like:” We still have to catch up with you in many domains but from now on we intend to deal with you on an equal footing basis. …While Xi Jinping is the most powerful Chinese leader since Mao, is his grip on power already beyond the risk of a backlash or not and how far are we from a fully stabilized power landscape in Beijing? ● China’s high nominal GDP growth rate is not necessarily a good sign. It arises from an eventually unsustainable system that has already taken China’s total debt to about 250 percent of GDP while continuing on a path to much higher levels. Much of this debt has been contracted in the course of building enormous excess capacity in the real estate, manufacturing, and infra-structure sectors. Since excess capacity does not generate income for the paying off of debt, the debt load will eventually be shifted to some sector capable of paying. ● Regardless of how it is paid, a shift in the structure and direction of the economy would entail at least a temporary slow-down of the Chinese economic growth rate to something like 3-6 5 GDP growth. Such a reduced growth rate would actually be a positive sign. However, because it would be seen negatively by many, and because it would be costly to vested interests, there will be enormous opposition to taking the steps necessary to achieve the temporarily slower growth rate. ● This is obviously a crucial moment in China, during which a number of shifts are occurring, with major implications for the country itself as well as for the global economic and geopolitical balance. ● While trying to decipher the developments it is important for decision-makers and China watchers to think outside the usual obsolete templates of “moderates” and “hard-liners” “reformists” and “conservatives” which serve only to blur the picture and distort judgment. The present reality in Beijing is too complex to be encapsulated in simplistic labels.

- This is the start of a new ball game in dealing with China. It will keep us on our toes for years to come.

Understanding China and Asia

By Shlomo Maital

Bilahari Kausikan

One of the wisest persons I know is Biliahari Kausikan, formerly Permanent Secretary of Singapore’s Foreign Ministry, and now Ambassador at Large. He has an exceptionally clear view of global and Asian geopolitics; I’ve been ranting and nagging him for years to write a book, or at least a regular blog.

Here, for my readers, is an excerpt from his recent document “A World in Transformation”.

The world is undergoing a profound transition of power and ideas. The modern international system was shaped by the West who prescribed its fundamental concepts, established its basic institutions and practices and influenced all major developments. That era is now drawing to a close. No one can predict the future and we do not know what will replace the western dominated system. But we can at least glimpse some of the issues that will have to be confronted.

Washington and Beijing are now groping towards a new modus vivendi. Neither finds it easy and establishing a new equilibrium will be a work of decades and not just a few years. Sino-US relations are already the most important bilateral relationship for East Asia, setting the tone for the entire region. As the 21st century progresses, Sino-US relations will become the most important bilateral relationship for the entire world influencing almost every aspect of international relations, just as US-Soviet relations did during the Cold War.

The Chinese government and people are rightly proud of what they have achieved. Never before in history have so many people been lifted out of poverty in so short a time. Still it would be a dangerous mistake to try to understand the global and regional transitions that are underway by simplistic slogans such as ‘Asia rising, the West declining’ as some Chinese intellectuals and even some officials occasionally come close to doing. The changes in the distribution of power that are occurring are relative not absolute. The global patterns of trade, finance, investments and production chains that have evolved as a result of East Asian growth cannot be characterized by geographically defined dichotomies. Many economic roads now pass through China and many more will in the future. Nevertheless the final destination is still more often than not the US or Europe. China is certainly rising. But it is always a mistake to believe one’s own propaganda and the west and in particular the US is not declining. All who have underestimated American creativity, resilience and resolve have had cause regret it.

Two competing visions of regional order are in play: a Sino-centric vision built around the ASEAN plus Three (APT) forum which comprises the ten Southeast Asia states with China, Japan and South Korea, and a broader and more open architecture built around the East Asia Summit (EAS) which is the APT with the addition of the US, Russia, India, Australia and New Zealand.

Given the growing centrality of East Asia in the world economy and the strategic weight of the US and China, the outcome of the debate over a new East Asian architecture will be the single most important influence on the global architecture of the 21st century. This is the strategic significance of what has been dismissed by western observers who do not really understand what they observe, as talk shops. No option has yet been foreclosed. Both the APT and EAS are experiments. But China’s preference is clear.

Singapore’s Prime Minister Looks Ahead Two Decades

By Shlomo Maital

After many visits to Singapore, I’ve come to appreciate the highly intelligent, competent political leadership, and capable civil service, this small nation enjoys. (And, by the way — good-looking!)….

Prime Minister Lee Hsien Loong, son of founding leader Lee Kwan Yew, is a Harvard graduate and highly articulate. Recently, he delivered an address, “Scenarios for Asia in the next 20 years”; here is a summary.

“Since the end of the Cold War, Asia’s strategic weight in international affairs has grown. It is home to more than half of the world’s population, and its share of global GDP has risen from one fifth to one third. This morning I will talk about both the clear trends and the critical uncertainties in Asia over the next 20 years. The key players will still be the US, China and Japan.

“Let me begin with the US. Today it is the dominant global power. In the Asia-Pacific, US power and influence have underpinned regional security and stability since the Second World War, and enabled all countries to prosper. The US has been a benign and constructive power, which explains why it is still welcomed by countries in the region. The Obama administration’s “rebalancing” towards Asia reflects the American strategic view, that the US has been and always will be a Pacific power. Unfortunately, the strains of being the global policeman have taken their toll on the US. The wars in Iraq and Afghanistan have cost the US more than 50,000 soldiers killed or wounded . The American people are naturally war weary. They are reluctant to engage in new fights or take on fresh burdens, whether in Syria, Ukraine or Asia. Its adversaries sense this, and harbor hopes that the US has lost the will to advance its interests and defend its “red lines”.

“I believe that in 20 years’ time, the US will remain the world’s pre-eminent superpower. China’s GDP will probably exceed America’s in absolute terms, but not in per capita terms. The US will still be the world’s most advanced economy, leading the way in innovation, technology and talent. I expect the Fortune 500 global list to include many new American companies which do not yet exist today, just as neither Google nor Facebook existed 20 years ago. Shale gas will enhance the competitiveness of US industries, and could also be an additional tool of American diplomacy. The US armed forces will still be the most formidable and technologically-advanced in the world.”

“There are two key uncertainties … The first is how soon Americans get over the current mood of angst and withdrawal, and regain the confidence and will to advance American interests around the world. The second is when the US can get its politics to work. Politicians on both sides need to come together to overcome the present gridlock and forge a consensus on the way forward, rather than be mired in partisanship and fundamental disagreement.”

Lee’s key point: The U.S. must continue its role as the world’s superpower/babysitter/democracy advocate. If it turns insular and fails in this role, the world will be a mess. To succeed in this role, America must regain its self-confidence, and fix its gridlocked political system.

Keep in mind – Singapore is tightly linked to America, economically and politically, and has enormous interests in America continuing to play a key role in Asia. So part of PM Lee’s speech is wishful thinking, and part is analysis. Let’s hope his optimism is based on analysis, not just hope.

Today is Memorial Day in America. In a memorial ceremony, the names of some 50,000 American casualties since 9/11 are being read. Years ago, the names of the 58,000 U.S. soldiers killed in Vietnam were read; it took three whole days non-stop. If America is tired of policing the world, one can understand. It matters for all of us, and our children and grandchildren, whether America will have the energy and spirit to continue to act for the world’s interests, not just America’s – and whether America will have the wisdom to intervene wisely, much more wisely than its interventions in Iraq and Afghanistan.

How America Buried Its Future in Its Defense Budget

By Shlomo Maital

In Thomas Friedman’s New York Times column, March 31, he writes about his cruise on the U.S.S. New Mexico, a modern nuclear attack submarine, underneath the Arctic ice cap.

He describes: “Excellence…if anyone turns one knob the wrong way on the reactor or leaves a vent open, it can be death for everyone. …As one officer put it: ‘You become addicted to integrity’. There is zero tolerance for hiding any mistake. The sense of ownership and mutuality and accountability is palpable.”

How many American companies would LOVE to be able to describe themselves as Friedman describes the U.S. Navy submariners? How many would LOVE to have world-class cutting-edge technology, like the U.S. Navy, far beyond that of other companies? Why don’t they? Because the U.S. defense budget in 2014, despite cuts, will total $526.6 b., or 4 per cent of America’s GDP. This is fully one-third of all the world’s defense spending in 2014, or $1.538 trillion, up from $1.538 trillion in 2013, the first rise in global defense spending in a decade. America is burying its economy in those costly nuclear subs.

Years ago, I visited an aircraft carrier, the U.S.S. Theodore Roosevelt. 11 decks of amazing technology and 5,000 superbly trained 18-year old or 20-year-old sailors. Planes launched and retrieved, at night, in darkness, simultaneously. Microsoft, IBM, eat your heart out.

America’s chief rival, China, spends only $132 b. a year on defense, or one-fourth that of America. And NATO? The 28 NATO nations have agreed they should spend 2 per cent of GDP on defense (half of America’s level), but none except the U.K. (2.4 per cent) actually do.

And Russia? Russia will boost its military spending by 44 per cent in the next three years, to fulfill Putin’s vision of a Great Russia (“bring back the U.S.S.R.!”).

So to sum up: The world is again in an arms race, defense spending is rising, and we are wasting huge sums on things like nuclear subs. Europe, as always, is sheltering under America’s defense spending, and has nothing to face Russia with. America has sunk its economy in military technology, which despite myths does not translate into cool civilian technology, for the most part.

* What purpose do those superb Navy subs and aircraft carriers serve, when the main threat to America is Taliban terror, al Qaida fighters armed with AK-47’s and home-made improvised explosive devices?

* Would the world be a better place if America’s economy were made stronger by diverting defense spending into infrastructure and civilian technology and education?

* Should Europe quit sponging off America and spend to defend itself?

* Is Russia again going to impoverish itself by putting billions into defense rather than rebuilding its flagging civilian economy, just as the U.S.S.R. did, fatally? Russia’s Siberia oil production is declining because Russia simply is not maintaining its oil infrastructure there – this, despite piles of cash in the bank. Simple incompetence.

Stay tuned.

What is Helping the Dollar Defy Gravity?

By Shlomo Maital

What in the world is helping the U.S. dollar defy gravity, keeping it from falling relative to other currencies? The U.S. economy’s recovery is weak, job creation is awful, President Obama is incompetent, the Congress is deadlocked, and America is turning inward, or returning to its traditional isolationism. Moreover, the Fed continues to print dollars (by buying $85 m. worth of Treasury bonds monthly). There is an enormous overhang of printed dollars out there.

China has lots its appetite for buying dollars. According to Floyd Norris (New York Times, Feb. 22-23/2014), China bought a net $48.5 b. worth of U.S.Treasury bonds last year. This is $20 b. less than in 2012. China now holds $1.27 trillion in Treasury bonds; together with Japan, this amounts to 42 per cent of the total $5.8 trillion in Treasuries held by all foreigners.

There is a great science fiction plot here. What if those foreign Treasury holders decided to spite the U.S. by dumping their dollar holdings? The dollar would crash, stock markets all over would drop, and an enormous crisis would result. Why would anyone do this? Well, America has plenty of ill-wishers out there. The fact is, the fate of the dollar, and the U.S. economy, is now in the hands of Chinese, Japanese and others, who hold vast amounts of U.S. assets.

By great good fortune, just as China is easing off its dollar purchases to support the dollar, Japan, under Abe and his “Abe-nomics”, has stepped up its buying. Japan bought a huge $71.3 b. in Treasuries in 2013, up from $53 b. in 2012. Japan is now the single largest purchaser of dollar assets. Of course, Japan does this to weaken the yen and help its exports. So far, it isn’t working too well.

It is significant that the American public, including the banks, slashed their holdings of U.S. treasuries. Clearly everyone knows that interest rates aren’t going down, they’re going up, which means Treasuries are going down, which means we should be selling them. Apparently, foreigners are more bullish about the dollar than Americans are. Not a good sign.

Right next to Norris’ column is an account of Fed discussions during the 2008 crisis. It is very disturbing. It shows how clueless the Fed Open Market committee was, especially after the Lehman bankruptcy, and how the Fed continued to worry about inflation, when the pressing problem was in fact deflation. It seems that not only are there no competent political leaders left in power, there are no competent economic and financial leaders either.

Can China Conquer Its Mountain of Money?

By Shlomo Maital

During the global financial crisis, China’s economy should have been hard hit. As Western economies’ demand for exports collapsed, China should have imploded. But it didn’t. After a short pause in its growth, the near-double-digit growth resumed.

One reason? China’s Central Bank rapidly and massively expanded the money supply, making credit exceptionally cheap and easy to get. China’s money supply (M2) grew by 30 per cent at the end of 2009. Credit growth has slowed but is still very rapid. M2 grew by 13.6 percent last year, about the same as in 2012 (13.8 per cent).

Overall, the amount of money in China has tripled since the end of 2006. One result has been to create a huge housing bubble and asset inflation. Hence, buying a very modest apartment in Wuhan, reports Keith Bradsher, in the Global New York Times, now costs about $100,000, or 14 years of pay at $575 / m. for an average industrial worker. Unaffordable.

In the U.S. and U.K., central banks created easy money (quantitative easing) by buying bonds, thus injecting reserves into the system. It was only partly effective, because banks chose to hold on to the cash rather than lend it, to shore up their ravaged balance sheets.

In China, monetary policy works differently. China buys huge amounts of U.S. dollars and Treasury Bonds and Bills, in return for renminbi, to keep the renminbi from growing stronger, and to maintain its undervalued exchange rate at about 6 RMB per buck (it probably be around 3.5, based on purchasing power). This keeps China’s exports cheap. Currency manipulation is illegal, but – not much can be done. If the U.S. screams too loudly, its multinationals will use their valuable cheap production sites in China and Apple, for instance, could cease to exist.

The problem China now faces? How to rein in that mountain of money, and keep it from generating inflation, or keep the housing bubble from bursting when the mountain starts to shrink (or grow more slowly)? America has failed at a much smaller task – ending Wall St.’s addiction to quantitative easing and free money. Will China do better? We should all watch China closely, and hope that wily Zhou Xiaochuan, longtime People’s Bank of China governor, will succeed. If he fails, we will all feel the pinch.