You are currently browsing the tag archive for the ‘debt’ tag.

The Great Money Mystery—Solved!

By Shlomo Maital

There is a major economic mystery in Israel, US and the West.

Governments are running big budget deficits, printing mountains of money, and yet – there is still virtually no inflation, while the inequality of wealth and income has grown alarmingly.

Why? And — should we worry?

I spoke with my friend Arie Ruttenberg about this. Ruttenberg built Kesher Barel into Israel’s largest advertising agency, sold it to the global McCann-Erickson, founded Club 50 and sold it to Migdal, and wrote a book about creativity with me [Cracking the Creativity Code, 2014]. He has expanded his assets through clever, at times contrarian, investments. Here is his ‘take’ on this mystery. It takes him 1,267 words to explain – double the length of my usual blog. I hope your investment of time is worth it. I’m pretty sure it is.

“In the old economy, the money that reached the marketplace was spread among everyone. When they used the money to buy goods, prices rose and this led to inflation. In the new economy, the money reaches only a few of the very rich, who mainly buy stocks, bonds and real estate. These are not included in standard measures of inflation, therefore it seems like there is no inflation.”

“Lately, Donald Trump, US President, has boasted about his ability to flood the system with limitless amounts of money and without causing inflation. Really? How can this be understood? There have been a few explanations of this phenomenon, that on the face of it contradict the Keynesian economic model: Huge budget deficits, together with an expansionary monetary policy and zero interest rates, and all this with full employment…and no inflation. A true economic miracle, that invites other politicians, including some among the Democrats, to offer the nation a Paradise on Earth, of unlimited prosperity through printing money. How did this happen? Is this really sustainable? Or, is it an illusion, with inflation hidden and disguised as something else? And is there a ticking time bomb, very very quiet, a social ‘bomb’ that will result in a deafening explosion soon?”

“A common explanation for this phenomenon is linked to globalization and technology. The argument is that we are at the dawn of a new macro-economic age, based on enormous global productive capacity and perfect competition through digital trade accessible for all. This explanation is only very partial, because it fails to explain why huge amounts of printed money enter the market and ‘evaporate’ without causing any increases in prices.”

“My argument is that the budget deficits and the monetary expansion indeed have had an enormous impact, but in contrast with the past, they have not caused significant inflation in consumption goods, but instead have mainly brought a rise in the price of equities, bonds and commercial real estate, which in turn increase economic and social inequality.

“John Maynard Keynes’ model assumes a uniform economy in which all consumers have similar preferences and compete for the same goods and services, available in limited quantities in the consumer goods markets. In this case, any additional money in the hands of consumers competes for the given amount of goods and so necessarily causes a rise in prices.

“I propose that we think about consumers, in terms of two groups: a) owners of capital and b) those who earn a living by their labor. Owners of capital earn far more than they need for their subsistence, and they save the difference, mostly by investing in equities, bonds and commercial real estate. These investments continue to expand their incomes, from year to year, but the added income does not necessarily increase their consumption, which is already very high. The second group, wage-earners or free-lancers who make a living from their wages, spend nearly all their income on their subsistence, and their savings are mostly targeted toward their pensions – that is, future consumption. Ultimately those savings will be almost completely eroded in value.

The gap between the two groups continues to grow over time, and continually increases the degree of inequality between them.

“What happens to the economy when the government vastly expands the amount of money? Or when the Central Bank creates huge amounts of credit at zero interest rates?

“The answer is: Most of the money and credit flows into the hands of the owners of capital, who grow wealthier as their assets expand, and as they continue to grow their wealth and create more jobs for wage-owners, until the economy reaches full employment. The wealthy grow even wealthier and those who live on their wages earn only enough to barely survive. In this way, the economy reaches full employment, but income and wealth inequality grow.”

“If the demand for workers grows, why don’t wages rise? Because of the two new phenomena I mentioned, globalization and technology. Through those two forces, we have turned the majority of workers into commodities – that is, into a basic good that has cheap plentiful substitutes. These two forces create a situation in which the supply of labor becomes almost infinite — in economists’ jargon, perfectly elastic. Therefore, when the owners of capital expand their businesses and assets, they do so almost without raising wages at all. When there is full employment, you can always hire cheap foreign workers.

“And why doesn’t the fall in unemployment bring a major increase in the demand for consumer goods and hence, a rise in their prices?

“Because of the same two reasons — globalization and technology. Workers can today buy cheaper goods anywhere on earth, via the Internet, and the supply of such goods is becoming nearly infinite. In this way, inflationary pressure in the goods market is prevented.

“Why doesn’t the rapid growth in incomes of the owners of capital cause inflation, when they spend that income?

“There are two reasons. First, because wealthy capitalists cannot eat two steaks for breakfast; and second, because it does cause inflation, but it is not called inflation, it is called “a rise in the stock market” and “a rise in the price of commercial real estate”. Yes, the excess demand caused by the budget deficit and cheap credit creates strong inflation in the main “goods” that the wealthy consume, but because these rises in equity prices and real estate prices are not included in the consumer price index, it is regarded as part of economic prosperity, and not as inflation.”

“Why do the wealthy people continue to buy stocks, bonds and real estate after they have become so costly?

“Because the rate of interest is zero, and because there are no other investment opportunities. Thus, the wheel continues to turn, over and over, never stopping, when: a) the wealthy grow more and more wealthy, pocket trillions of dollars of wealth, and feel super-rich; and b) the wage-earners enjoy full employment, stretch their income to last the full month, and are content. This can be described as the “happiness of the poor”; c) the politicians waste money endlessly and are pleased with themselves; d) the governments expand the debt they owe and nobody cares; e) the central banks expand their balance sheets, and again, nobody cares. Hallelujah! The messiah has come!

“Can this go on forever? There is no reason why not, on condition that: a) a few madmen do not arise and start to complain about the social inequality that is becoming unbearable; b) a ‘crazy’ US Central Banker does not appear who starts to raise interest rates, and thus puncture the stock markets, bond markets and real estate prices; c) a stupid American President does not appear who crushes globalization, imports of cheap goods and imports of cheap foreign labor, through trade wars.

“Then, what happens to the global economy? It becomes an economy of rich feudal lords, and contented vassals who earn exactly as much as they need to go to bed with a full stomach, get up the next morning and to serve their lords. Is this what Paradise looks like? No, this is what the economics of wealth inequality looks like.

“At the end of the 1970’s, Israel had a cabinet minister who used the phrase “blessed inflation”, to describe the impact of influence on accelerating economic activity – until, that is, the inflation destroyed the Israeli economy. When the US President brags about flooding the American economy with money in order to create growth, he is boasting in fact about “increasing blessed inequality”.

“How long will this last? Heaven knows”.

Ballooning Debt & Deficits: How the Republicans are Making America “Great (in Debt)” Again

By Shlomo Maital

You, dear reader, are as tired of reading about the Republicans’ iniquities as I am of writing about them. Hopefully – this is the last blog on the subject for a very long time.

The Trump Administration has made hypocrisy an essential element of everything they do, with unqualified support of Republicans, both in the House of Representatives and the Senate.

The latest 2-year budget? It calls for massive spending increases in defense and non-defense items, without showing how to pay for them. Add this to the unfunded tax cut. The result?

* The ratio of debt to GDP will rise to 109% by 2027, and

* the spending bill will add $1.2 trillion to the deficit by 2019.

Under Obama, the Republicans rioted over Obama’s free-spending budgets. But it is a fact – deficits have risen far more under Republican presidents (remember Reagan’s tax cuts, unfunded?) than under Clinton and Obama. Clinton in fact balanced the budget! Obama ran a small deficit.

Make America great again? Here is how Trump is doing that.

Here is the list of countries with triple digit (over 100%) debt to GDP ratios: Portugal, Italy, Eritrea, Belgium, Mozambique, Japan.

You’ve done it Trump! You have managed in just one year to help America gain entry, very soon, to this unique club of great nations, with GRRRREAT debt to GDP ratios. America will soon drown in debt, on the Republicans’ watch. Does this bring new meaning to the word “political hypocrisy”?

I predict this Trump Tweet: GREAT world-leading debt ratio. Historical. Fabulous. Debt is great. I know — I did borrow and then bankrupt. Watch me bankrupt America too…piece of cake. Make America broke.

“Drowning in Debt”

By Shlomo Maital

A new report from McKinsey Global Research, “Global Debt: Challenges and Opportunities”, sounds the alarm, from a rather unlikely source – a consulting company that makes its living on optimism and activism.

Here is what McKinsey says, worth heeding!

”The world is deep in a flood tide of debt. Do we care and what do we do about it?

….More than 8 years since the 2008 global financial crisis started the world seems to be drowning in debt. Global economic growth remains anemic..some economists attribute it to the high level of debt (govt., businesses, households have been devoting significant resources to debt servicing instead of productive activities). …Global debt has been growing faster than the economy… as of mid 2015 it stood at 294 % of global gross domestic product, up 25 percee end of 2007 and 48 percentage points since the end of 2000. In many countries debt has increased to levels not normally seen during peacetime in advanced economies.”

The world has painted itself into a corner. Advanced economies desperately need major investments in infrastructure and human capital. Instead they are either a) slashing public spending, to try to control the high level of debt, or b) recycling huge debts, borrowing new money just to pay off old money, because slow growth has put the brakes on tax revenues and increased deficits.

I see little sign of creative thinking to solve the problem. Central Bankers recently meet at Jackson’s Hole, Wyoming, took off their ties and formal dress…. And heard Janet Yellen, head of the US Fed, speak about how she plans, maybe, perhaps, to raise interest rates a bit this year. In Europe the central bank continues to push negative interest rates, after everyone knows for sure that you cannot get out of the painted corner solely by adding to the already huge mountain of money.

Does anyone have a creative idea? Our central bankers are completely out to lunch… literally.

Euro Nations: Benchmark Estonia

By Shlomo Maital

With all eyes focused on Greece, it is easy to forget about little Estonia. Bloomberg Business Week reports that this tiny nation, squeezed between Latvia and Russia, joined the Euro zone only four years ago. Many countries leaped at the Euro capital markets opportunity and their governments sold bonds like drunken sailors.

Not Estonia. Government debt is less than 10 per cent of GDP. That is one – tenth the average debt burden in Europe, and about 1/20th the debt burden of Greece (170 per cent of GDP).

How come?

Estonia has refrained from issuing government bonds, since 2002. Instead, the Estonian government took loans from the European Development Bank, which lends ONLY for infrastructure and investment, not to finance current government spending. Maris Lauri says, “we can’t afford to borrow to finance current spending; such borrowing becomes a habit and we saw where that landed Greece and Russia, in 1997/8”.

Some Estonian economists are opposed. They think Estonia should leap at the low interest rates and borrow. But it won’t happen.

“Estonia is a strange bird in the Euro zone,” says Frederick Erickson, who heads the European Institute for Political Economy in Brussels. “No other country has such a stronge instinct for understanding the way macroeconomic problems are rooted in the real economy.”

Estonia’s Prime Minister says Estonia has to save its borrowing and access to Euro capital markets, for the time when Estonia’s GDP reaches 75 % of the Euro average (it is now 73%), at which time European aid money dries up.

Strong wise leadership can keep a small country like Estonia out of hot water. Greece, in deep hot water, has to be rescued. Estonia will not. As the Hebrew saying goes, wise leaders avoid crises that smart leaders know how to escape from.

What’s Wrong with the World? Ask Paul Krugman..and Road Runner

By Shlomo Maital

Remember the Road Runner cartoons? Wile E. Coyote continually is duped into running off very high cliffs by the clever elusive Road Runner.

Well, I think this captures the advice economists have been giving policymakers worldwide, as the world economy again weakens (according to the IMF). We keep running off the cliff, like Coyote. And for evidence, I call to the stand Nobel laureate and New York Times columnist Paul Krugman. I will quote Krugman’s latest Op-Ed, (Oct. 12), it is rather lengthy, but provides a clear accurate and fairly concise diagnosis. It causes me to lose sleep – it may do the same to you too, so…beware, before you read on. Krugman’s words are in quotation marks. Again, this analysis is long – but essential, if you want to really understand what in the world is going on: [If you want to stop here, and seek a one – sentence summary: We’re being killed by high debt, we need to forgive it, wipe it out and start fresh – there’s no other way].

- Analysis: Where we stand: “The world economy appears to be stumbling. For a while, things seemed to be looking up, and there was talk about green shoots of recovery. But now growth is stalling, and the specter of deflation looms.”

- We’re fulfilling Einstein’s definition of insanity: Doing the same thing and expecting different results. “If this story sounds familiar, it should; it has played out repeatedly since 2008. As in previous episodes, the worst news is coming from Europe, but this time there is also a clear slowdown in emerging markets — and there are even warning signs in the United States, despite pretty good job growth at the moment.”

- But WHY are we in this mess, that began 6 years ago? “Why does this keep happening? After all, the events that brought on the Great Recession — the housing bust, the banking crisis — took place a long time ago. Why can’t we escape their legacy? The proximate answer lies in a series of policy mistakes: Austerity when economies needed stimulus, paranoia about inflation when the real risk is deflation, and so on.”

- What is the basic problem? “What, after all, is our fundamental economic problem? A simplified but broadly correct account of what went wrong goes like this: In the years leading up to the Great Recession, we had an explosion of credit (mainly to the private sector). Old notions of prudence, for both lenders and borrowers, were cast aside; debt levels that would once have been considered deeply unsound became the norm. Then the music stopped, the money stopped flowing, and everyone began trying to “deleverage,” to reduce the level of debt. For each individual, this was prudent. But my spending is your income and your spending is my income, so when everyone tries to pay down debt at the same time, you get a depressed economy.”

- What can be done? “Historically, the solution to high levels of debt has often involved writing off and forgiving much of that debt. Sometimes this happens explicitly: In the 1930s F.D.R. helped borrowers refinance with much cheaper mortgages, while in this crisis Iceland is outright canceling a significant part of the debt households ran up during the bubble years. More often, debt relief takes place implicitly, through “financial repression”: government policies hold interest rates down, while inflation erodes the real value of debt. What’s striking about the past few years, however, is how little debt relief has actually taken place. Yes, there’s Iceland — but it’s tiny. Yes, Greek creditors took a significant “haircut” — but Greece is still a small player (and still hopelessly in debt). In major economies, very few debtors have received a break. And far from being inflated away, the burden of debt has been aggravated by falling inflation, which is running well below target in America and near zero in Europe. Why are debtors receiving so little relief? As I said, it’s about righteousness — the sense that any kind of debt forgiveness would involve rewarding bad behavior. In America, the famous Rick Santelli rant that gave birth to the Tea Party wasn’t about taxes or spending — it was a furious denunciation of proposals to help troubled homeowners. In Europe, austerity policies have been driven less by economic analysis than by Germany’s moral indignation over the notion that irresponsible borrowers might not face the full consequences of their actions. So the policy response to a crisis of excessive debt has, in effect, been a demand that debtors pay off their debts in full. What does history say about that strategy? That’s easy: It doesn’t work. Whatever progress debtors make through suffering and saving is more than offset through depression and deflation. That is, for example, what happened to Britain after World War I, when it tried to pay off its debt with huge budget surpluses while returning to the gold standard: Despite years of sacrifice, it made almost no progress in bringing down the ratio of debt to G.D.P.”

- So, how do we move ahead? “A recent comprehensive report on debt is titled “Deleveraging, what deleveraging?”; despite private cutbacks and public austerity, debt levels are rising thanks to poor economic performance. And we are arguably no closer to escaping our debt trap than we were five years ago. But it has been very hard to get either the policy elite or the public to understand that sometimes debt relief is in everyone’s interest. Instead, the response to poor economic performance has essentially been that the beatings will continue until morale improves. Maybe, just maybe, bad news — say, a recession in Germany — will finally bring an end to this destructive reign of virtue. But don’t count on it.”

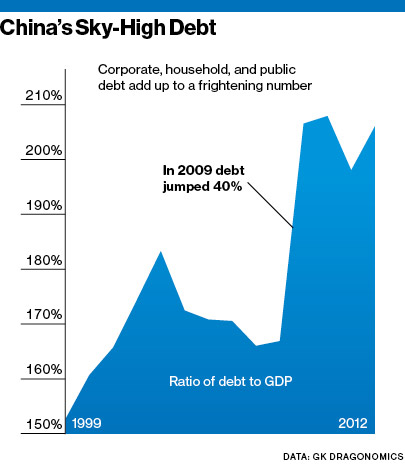

China: Big Nation, Big Worries

By Shlomo Maital

A new survey shows that half of Americans believe the recession is still alive and well, despite the booming stock market. And close analysis shows that the world’s second biggest economy, China, also has big worries. So when the world’s two largest economies are struggling, global managers need to be on their toes, to daily track events and manage risk.

My friend Clyde Prestowitz, formerly President Reagan’s trade advisor and now head of Economic Strategy, has provided us with some quality insights into China’s current predicament. “This is the start of a new ball game with China,” Clyde warns. Here is a summary:

- Xi Jinping’s two major goals are: 1)Restore the power of the center and ensure the sustainability of the Party’s rule. 2) Restore China to its historical position of prominence of the world stage. This marks a departure from the line of Deng Xiaoping who urged : “observe calmly, secure our position, cope with affairs calmly, hide our capacities, bide our time, maintain a low profile, and never claim leadership.” ● Two schools of thought now contend in Beijing – one advocating the low profile approach, the other saying that this low profile has encouraged Japan and other Asian countries to push their claims in the North and South China Sea, and arguing that it is now time to show a more assertive posture. ● Xi seems clearly to be leaning toward this latter approach: What he is now basically saying to the US is rather something like:” We still have to catch up with you in many domains but from now on we intend to deal with you on an equal footing basis. …While Xi Jinping is the most powerful Chinese leader since Mao, is his grip on power already beyond the risk of a backlash or not and how far are we from a fully stabilized power landscape in Beijing? ● China’s high nominal GDP growth rate is not necessarily a good sign. It arises from an eventually unsustainable system that has already taken China’s total debt to about 250 percent of GDP while continuing on a path to much higher levels. Much of this debt has been contracted in the course of building enormous excess capacity in the real estate, manufacturing, and infra-structure sectors. Since excess capacity does not generate income for the paying off of debt, the debt load will eventually be shifted to some sector capable of paying. ● Regardless of how it is paid, a shift in the structure and direction of the economy would entail at least a temporary slow-down of the Chinese economic growth rate to something like 3-6 5 GDP growth. Such a reduced growth rate would actually be a positive sign. However, because it would be seen negatively by many, and because it would be costly to vested interests, there will be enormous opposition to taking the steps necessary to achieve the temporarily slower growth rate. ● This is obviously a crucial moment in China, during which a number of shifts are occurring, with major implications for the country itself as well as for the global economic and geopolitical balance. ● While trying to decipher the developments it is important for decision-makers and China watchers to think outside the usual obsolete templates of “moderates” and “hard-liners” “reformists” and “conservatives” which serve only to blur the picture and distort judgment. The present reality in Beijing is too complex to be encapsulated in simplistic labels.

- This is the start of a new ball game in dealing with China. It will keep us on our toes for years to come.