You are currently browsing the tag archive for the ‘paul krugman’ tag.

One-Armed Nobel Candidate Economist Is Fired

By Shlomo Maital

Paul Romer Paul Krugman

Every day, members of my profession, economists, find new ways to make me deeply regret I ever became one. The latest episode is a story of two economists named Paul.

President Harry Truman, the US President who suddenly and unexpectedly took office when President Roosevelt died in 1944, once said famously: “Give me a one-handed economist! All my economists say, ‘on the one hand…and, on the other’”.

Economists respond: “Give me a break, Truman! We are objective professionals. Our job is to offer alternatives and explain the implications of each. YOU are an elected official. We are your servants. YOU are the one elected by the democratic process to choose and decide, not us! We simply show you the choices.”

I myself used to repeat that mantra, during a year as head of an Israeli government planning body. But I soon learned – reality is different. When economics is a value-free zone, it is useless to political leaders. State your values, state your position, clean up the jargon, speak in ordinary language, and keep one hand anchored deeply in your pocket.

The Guardian now brings us a shocking, infuriating episode in which a future Nobel economist is fired for demanding clarity and truth. The economist is Paul Romer. In his Ph.D. dissertation, he built a powerful new theory now widely accepted, called “endogenous growth theory”. But another Paul, Paul Krugman, a Nobel laureate, has for over two decades been a beacon of clarity and one-armed economics.

In brief: Since MIT economist Robert Solow, we’ve known that half or more of all economic growth is caused by technological change. But Solow treated it as ‘exogenous’, outside the system. Romer observed that technological change is endogenous – it is created by what we do, in education, innovation, and R&D, etc. His two Journal of Political Economy articles published in 1986 and 1990, respectively, started endogenous growth theory and changed the world. He will win a Nobel Prize soon for this. It has changed the way everyone thinks about pro-growth policies and plans.

The Guardian: “The chief economist at the World Bank has stepped down from its research arm after staff were vexed by demands to write succinctly, including cutting superfluous uses of the word “and” in reports or emails. Paul Romer, 61, will leave the Development Economics Group (DEC), according to a staff announcement reported by Bloomberg. He had asked for shorter emails, while also cutting staff off if they talked for too long during presentations, it said. In response to press inquiries about internal “objections to my insistence on clearer writing,” Romer published writing guidance he had issued to DEC staff on a blog on Thursday. He said he suffered from dyslexia, making writing hard, but added “everyone in the Bank should work toward producing prose that is clear and concise. This will save time and effort for a reader. Thinking about the reader is an example of what I mean when I say that we should develop our sense of empathy.” Romer cut more US$1 million in annual expenses from the DEC budget, a body of more than 600 economists. But it appeared to be his attacks on convoluted, lengthy reports of that researchers took cause with. In an email to staff, Romer argued that the bank’s flagship publication, World Development Report, would not be published “if the frequency of ‘and’ exceeds 2.6 percent,” according to Bloomberg. He reportedly cancelled a regular publication that did not have a clear purpose.”

“Romer is credited with the quote “A crisis is a terrible thing to waste,” which he said during a November 2004 venture-capitalist meeting in California. Although he was referring to the rapidly rising education levels in other countries compared to the United States, the quote became a sounding horn by economists and consultants looking for a positive take away from the economic downturn of 2007–2009.”

Paul Romer wanted one-handed economists, who speak clearly, and paid the price. But is there a role-model for clear-thinking clear-speaking economics? There is. New York Times columnist Paul Krugman.

The Economist: “From a mono-manual perspective, at least, Harry Truman would have loved Paul Krugman, an economist who rarely hesitates to take a bold position—even when the subject is himself. In recounting the transformation of his twice-weekly New York Times column from a genial discussion of the “New Economy” into a widely read broadside against the Bush administration, the Princeton professor recently described himself as “a lonely voice of truth in a sea of corruption.”

Krugman has blasted Trump and the Republicans, and identified their scorn for economic truth.

In the 1930’s economics took a wrong turn. Influenced by the London School of Economics, economists decided to become like physicists and deal with only ‘pure science’, without ethical value judgments. At that moment, economics became irrelevant. And it remains so.

I hope Romer wins the Nobel Prize later this year. In his acceptance speech, I hope he tears several strips off the moribund walking-zombie economists there, hundreds of them, a whole building full of them at 1818 H Street in downtown Washington. That building is a wasteland desert, even though it is in the heart of Washington.

The Rich 1% Recovered; The Rest of Us Didn’t

Fat Cats: Let’s Have Another Bubble!

By Shlomo Maital

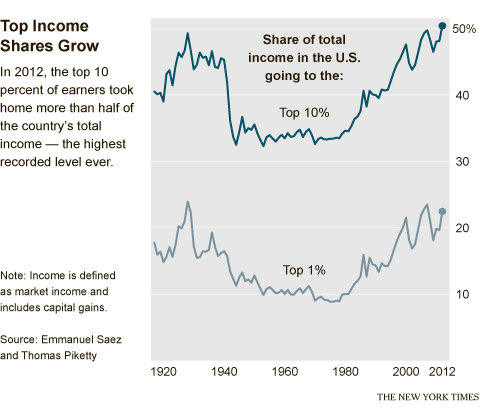

Paul Krugman’s New York Times column “Rich Man’s Recovery” draws our attention to Annie Lowrey’s New York Times blog Economix (Sept. 10). Using data from a study by French economists Emmanuel Saez and Thomas Pikkety, she shows alarmingly that for the U.S.:

* In 2012, the top 10 % of income earners took home more than half the country’s total income. This is the highest recorded level of inequality ever, higher even than in 1929! (Income includes capital gains).

* The top 1 % of income earners took home one fifth (20%) of all income, close to the previous record in 1929, and among the highest levels since 1913, when the income tax was imposed.

Recovery? It’s all gone to the fat cats. None to us, not even crumbs. That is why the ‘recovery’ is so weak and tenuous.

According to Lowrey: “The figures underscore that even after the recession the country remains in a new Gilded Age, with income as concentrated as it was in the years that preceded the Depression of the 1930s, if not more so. High stock prices, rising home values and surging corporate profits have buoyed the recovery-era incomes of the most affluent Americans, with the incomes of the rest still weighed down by high unemployment and stagnant wages for many blue- and white-collar workers.”

I would stress another related explanation. The U.S. Fed has fought the Depression with the only tool available, by printing scads of cheap money, lent at virtually zero interest. Directly and indirectly, this benefits the fat cats. But it hasn’t benefitted us ordinary people. Why? Because the goal of the Fed was to spur investment. But businesses aren’t investing, who needs to invest with demand so weak? Why is demand so weak? Because we don’t have money? Why don’t we have money? Because the fat cats have it. Why? Because they have quickly returned to the games that caused the financial collapse: financial manipulation, in place of real economic investments, leveraging cheap money. Not only that – by manipulating bond prices, they have panicked Fed Chair Bernanke into retreating from his plan to stop printing more and more and more money. If you think the Fed policy is independent, examine what happened when Bernanke just mildly hinted he might stop printing money. Wall St. slammed bond prices down, and stock prices – and Bernanke quickly backtracked.

The Fat Cats caused the crisis. We bailed them out. And now they’re back to their original games. They might as well all put this bumper sticker on their Porsche’s: “Hey…let’s have another bubble. Why the hell not?”