You are currently browsing the tag archive for the ‘euro’ tag.

Greece Collapses – Germany and the World Will Pay the Price

By Shlomo Maital

Two trucks speed toward each other on a deserted highway. They are 50 kms. apart. Each drives at 100 kms. an hour. They have 15 minutes before they meet. Plenty of time to slow down, stop, turn off the road.

Yet they still collide head on, with massive damage.

Then, the experts debate why this happened.

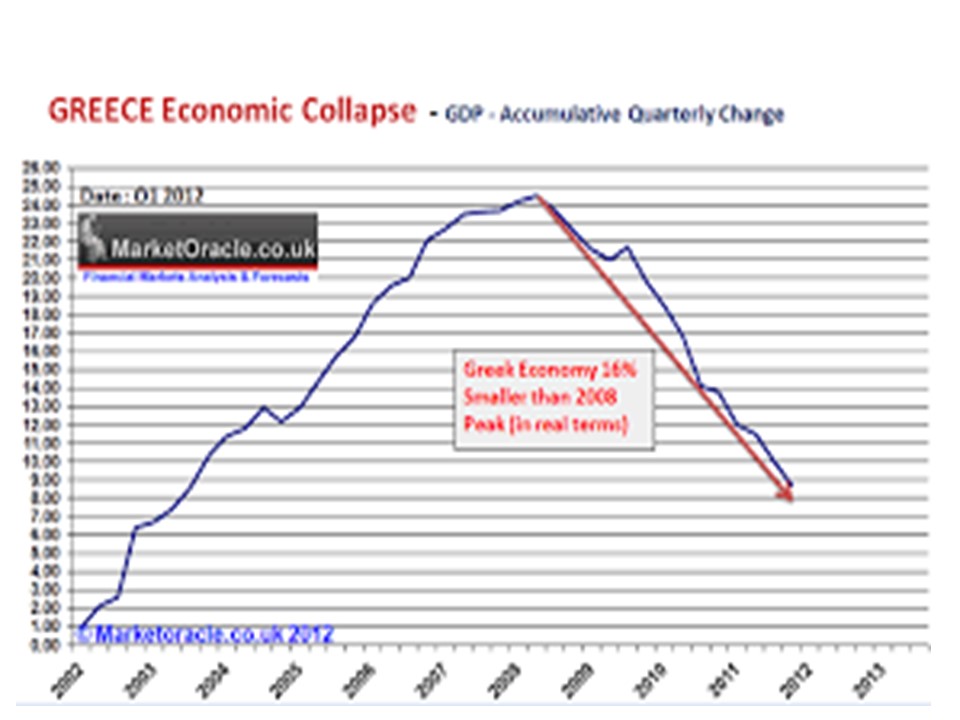

This is the story of Greece. Greece joined the EU in 1981. It joined the Euro in 2000, in time to implement paper euros and coins when all of Europe did.

Here is what former European Central Bank Chief Economist Otmar Issing said, in March 2011: “Greece was only able to join the euro through deception [its budget deficit was far above permissible levels] and the currency bloc’s leaders have been “too polite” ever since to deploy adequate sanctions that could have averted the region’s debt crisis. When I worked for the ECB, I suffered every time countries didn’t meet the criteria…Greece cheated to get in, and it’s difficult to know how we should deal with cheaters. … Greece will probably be unable to honor its debts as it grapples with insolvency. The country’s repayment ability remains questionable even after the government endorsed an accelerated asset-sale plan and a package of budget cuts necessary to draw a fifth tranche of its bailout.”

It was obvious in 2011, four years ago, that Greece could not pay back all that it had borrowed. Today its public debt is an unsustainable 177 percent of its GDP. So it is obvious – much of the debt has to be wiped out, one way or another.

Are Greece and its leaders to blame? Sure. But on the principle of “sunk costs”, the history is irrelevant. The question is, what to do today, to avoid the crash? We’ve seen it coming for years, according to Issing. Yet Europe and its blind leaders continued to torture Greece, imposing ever more severe austerity. You cannot grow an economy by shrinking it. And an economy can only pay back debt by growing. Grade 5 kids know that. But politicians and economists don’t. You cannot have a single currency, the euro, without a single united banking system throughout the euro zone with one set of rules. That never happened. It never will. So the euro will become a permanent chronic ongoing crisis, and it has been for years.

Yesterday German Chancellor Angela Merkel said, “if the euro fails, Europe fails.” Really? What has Chancellor Merkel done to recognize reality – Greece cannot, cannot, pay back its debt? She should have said, “The euro has failed, because I have failed, and I therefore tender my resignation. I failed to explain to the German voters, that even if we wipe out a quarter of Greek’s debts, Germany still has gained immensely”.

Who has been the big winner from Greece’s suffering? Germany.

Why? Because Greece has dragged down the external value of the euro, and the cheap euro makes German exports more competitive. If Germany under Merkel would give Greece 3 percent of all it has gained from the Greece-driven euro decline, the crisis would be over.

Some 37 % of Germany’s GDP comprise exports, or nearly $1.5 trillion (in 2014), just slightly behind that of the U.S., whose population is three times bigger. Even China exports only 23 % of its GDP. How strong will German exports be, when Greece leaves the euro, restores the drachma, bankrupts its citizens and its banks, crashes world financial markets, bashes the world economy — and then the euro soars, throwing Germany’s export-driven economy into recession?

Two trucks speeding toward each other for years. Could the crash have bene prevented? Sure, with common sense.

Was it?

No. History will be unforgiving to the hypocritical blind leaders who caused this.

Euro Nations: Benchmark Estonia

By Shlomo Maital

With all eyes focused on Greece, it is easy to forget about little Estonia. Bloomberg Business Week reports that this tiny nation, squeezed between Latvia and Russia, joined the Euro zone only four years ago. Many countries leaped at the Euro capital markets opportunity and their governments sold bonds like drunken sailors.

Not Estonia. Government debt is less than 10 per cent of GDP. That is one – tenth the average debt burden in Europe, and about 1/20th the debt burden of Greece (170 per cent of GDP).

How come?

Estonia has refrained from issuing government bonds, since 2002. Instead, the Estonian government took loans from the European Development Bank, which lends ONLY for infrastructure and investment, not to finance current government spending. Maris Lauri says, “we can’t afford to borrow to finance current spending; such borrowing becomes a habit and we saw where that landed Greece and Russia, in 1997/8”.

Some Estonian economists are opposed. They think Estonia should leap at the low interest rates and borrow. But it won’t happen.

“Estonia is a strange bird in the Euro zone,” says Frederick Erickson, who heads the European Institute for Political Economy in Brussels. “No other country has such a stronge instinct for understanding the way macroeconomic problems are rooted in the real economy.”

Estonia’s Prime Minister says Estonia has to save its borrowing and access to Euro capital markets, for the time when Estonia’s GDP reaches 75 % of the Euro average (it is now 73%), at which time European aid money dries up.

Strong wise leadership can keep a small country like Estonia out of hot water. Greece, in deep hot water, has to be rescued. Estonia will not. As the Hebrew saying goes, wise leaders avoid crises that smart leaders know how to escape from.

Explaining (again) the Euro/Greece Crisis to Grade 5

By Shlomo Maital

Hello Grade 5’ers! Thanks for inviting me. I know my subject, money and economics, is BOOOOOring. But believe me, it is important for you to know what is going on, because when you are just a few years older, what happens in Europe will affect you. Because Europe is the world’s biggest, or next-to-biggest, economy, depending on how you add the numbers.

So here’s the deal. Europe has had lots and lots of terrible wars, with France, Germany England and others fighting each other. Someone (in France) had a great idea. What if we stopped fighting and made money together, by buying each other’s stuff? If you buy my stuff, I’m not likely to want to fight you. So they called it the European Single Market. And it worked beautifully. No-one thinks Europe will have a big fight any time soon (though, Russia may be an exception – that’s another scary story).

If you sell and buy, you use money. But there are 28 countries that belong to this European club. What a mess if you have to start finding escudos, guilders, lira, pounds, francs, and all kinds of weird money. So 19 of the countries decided they would use the same new currency, which they called the “euro”. Kind of like America, where the 50 states all use the same money, the dollar. Some 332 million Europeans use the euro.

But there is a problem. If you have the same money, you have to have the same rules for making the money. That means, you have to get all those 19 countries to agree on the “rules of the game”. You can’t play baseball or football if neither team agrees what the rules are, right? And here is where things broke down.

Some countries want there to be lots and lots and lots of euros. Some countries want just a little bit of money. Some countries (like, a little country called Greece, only 11 million people) broke the rules, spent too much money, and got into trouble, just like we do when we spend too much. Because they had to borrow and now they have trouble paying back what they owe. Other countries, like Germany, who had lots of money, helped Greece but sent Greece kind of to the penalty box. No more spending. Less treats, less goodies. And Greece didn’t like it. I wouldn’t either.

So Greece has had elections and its new leaders are making a big fuss about the punishments other countries have given it. Some think Greece might even leave the ‘club’ (the euro). That might be terrible, because then some other countries might do the same, and the whole club would collapse. So, the 27 countries want Greece to stay in the club but they do not agree how to make that happen. It’s like, do you punish the Greek people for overspending (they didn’t do it, their leaders did)? Do you forgive them, and then others might do the same? Why should other countries give money to Greece? But if they don’t, they will lose too, because the whole Euro club might come apart.

And you know, Grade 5’ers, I guess you could see this coming. If you start a game, and you have not all agreed clearly on the rules, including for things that are really strange (like, what if two guys are on second base – who’s out? What if one player’s mother comes on the ice and drags him (the goalie) off to Hebrew School? (yup, happened to me) – you’re going to get into trouble. Those Europeans, they started a club without a clear set of rules, and worse, without any way of leaving it without causing REAL trouble.

I’m pretty sure they will muddle through and keep that weird euro club going. They all have too much to lose. But boy, kids, I think you Grade 5’ers could have done a far better job. Those Europeans, they couldn’t see their fingers even if they were right in front of their nose. So, when you go to play a game, or start a club, make sure everyone knows the rules. Kids usually do. It’s the grownups who are dumb about that sometime.

Switzerland: Why It Is Scaring Us

By Shlomo Maital

Last Thursday Switzerland did two scary things. Scary for me – many (except for forex traders, who got creamed) did not take much notice.

First, they cut the interest rate paid on bank reserves to MINUS 0.75 percent. Minus??? That means, deposit 1 million Swiss francs, at the end of the year you get back 992,500. Why? To discourage money from flowing in.

Second, most important, the Swiss Central Bank announced it would no longer maintain the exchange rate vis a vis the euro at no more than 1.2 Swiss francs per euro, a policy announced in 2011. It pegged its exchange rate, to keep the Swiss franc from getting too strong, because the euro was undergoing a series of crisis and losing value. And each time the Swiss franc goes up relative to the euro, it makes Swiss exports more and more expensive. In a surprise move, the Swiss now say they can no longer maintain this peg and the Swiss franc will be allowed to rise and strengthen, relative to the euro and of course relative to the dollar.

Switzerland is one of the world’s most solid stable countries with by far the world’s strongest currency. It is a safe haven – when things go wrong in the world, and they do all the time, money flees to Switzerland, buys Swiss francs and sits mostly unnoticed in vaults and bank deposits.

Why is a strong Swiss franc a problem? Because Switzerland’s main trading partners are in Europe. When its currency strengthens, its goods become expensive. Amazingly, despite the enormously high wages and costs in Switzerland, the Swiss run an export surplus, exporting $308 b. yearly (over 70 per cent of their GDP) and importing only 288 b. How do they do this? By making and selling branded goods, high quality, precision machinery, and by selling value rather than cost. But there is a limit.

What do we learn from Switzerland’s actions?

First, no country is an island. Europe is suffering from deflation, caused by absolutely stupid austerity policy. EU policies, by bringing Greece to its knees, brought the euro to its knees as well; because again Greece threatens to leave the euro, and once one country does it, many others may consider it. Switzerland is paying the price not for its own mistakes but for those of Europe.

Second, deflation. Economist Abba Lerner once said deflation (falling prices) is 100 times worse than inflation (rising prices). He may have underestimated deflation. The only way to dig yourself out of deflation is to stimulate demand. But Europe is doing the opposite. So Europe is now exporting its deflation to Switzerland. The rising franc will make imports cheaper, and lower prices in Switzerland. This will boost imports and hurt the economy, thus importing Europe’s folly to Switzerland against its will.

Why are the Swiss no longer pegging the franc at 1.2 euros? Because they no longer can. To do this the Bank of Switzerland has to buy very large amounts of euros, and sell francs, thus expanding the money supply. The Bank feels it can no longer continue to do this nad maintain Switzerland’s vaunted stability. Switzerland has an absolutely balanced federal budget, and always does, because the Central Bank has the final say on the budget, and sends it back to the legislature if it is too loose.

Columnist Paul Krugman thinks a “fresh wave of safe-haven money was making the effort to keep the franc down too expensive.” Imagine – you can ruin your country by causing money to flow out, but apparently, also, by causing too much money to flow in (like Switzerland). So far the Swiss have brilliantly reaped the benefits of trading with the EU without actually adopting the shaky, fragile, illogical currency called the euro. But there is no way that the European sickness cannot spread to Switzerland too. We learned that last Thursday.

This whole episode is scary, because it shows clearly that no matter how well run an economy is, and its money, it cannot avoid the collapse, deflation and folly going on around it. Sorry Switzerland. You live in a bad neighborhood. And you can’t really move those beautiful Alps to, say, the Caribbean.

Why Latvia Loves the Euro

By Shlomo Maital

Tomorrow, Jan. 1, Latvia becomes the 18th nation to adopt the euro, following Estonia’s euro adoption in 2011. A third Baltic nation, Lithuania, will adopt the euro in 2015.

Why would any country willingly choose to shift to a currency in so much trouble? It is simple, according to Richard Milne, writing in today’s Financial Times.

According to Finance Minister Andres Vilks, ““Russia isn’t going to change. We know our neighbour. There was before, and there will be, a lot of unpredictable conditions. It is very important for the countries to stick together, and with the EU. We have completed our mission” of joining all the main institutions in Europe from the EU to Nato….. “We will be more integrated and protected in case of troubles, and we can see what is happening in Ukraine today.”

Russia has exerted tremendous pressure on Ukraine, not to sign a free-trade agreement with the EU, and has supplied an enormous $14 b. loan as a tempting bribe.

The adoption of the euro came despite huge Latvian opposition to the idea, among the public. A poll last October showed only one Latvian in five favored the euro. The people of Latvia seemed to believe that along with the euro came austerity, which is partly true.

Vilks noted that Russia (and Putin) “is nervous about losing partners and influence. That is one reason why the Baltics and Finland were so eager to go to all institutions, including Nato. It’s not so easy for small countries to deal with these issues; we need help.”

According to Milne, Latvia still has close ties with Russia, with about 40 per cent of the bank deposits in the country coming from ex-Soviet states, while about a quarter of its population is ethnic Russian.

As a small nation, Latvia has little leverage on Russia. But, on the other hand, it also has little importance. Ukraine, a huge country, is crucial for Russia; Latvia is almost a ‘rounding error’.

Latvia’s euro adoption shows the importance of strong political leadership. How many Western political leaders would face a hugely unpopular decision, and proceed with it anyway, knowing they could well be tossed out of office in the next election. Kudos to Vilk and little Latvia. Obama, Netanyahu – do some homework on the Baltic states. They know things about leadership that neither of you do.