You are currently browsing the category archive for the ‘Global Crisis Blog’ category.

Matteo Renzi Revives Italy

By Shlomo Maital

The attention of the business press has been almost entirely focused on the bad-news story of Greece. While Greece suffers, almost un-noticed Italian Prime Minister Matteo Renzi, who took over in 2014, has fulfilled his promise to revive the Italian economy. He has cut public spending, slashed deficits, modernized the judicial system, and reformed the sluggish labor market. (All these reforms are equally vital in France – but Hollande is neither able nor willing to undertake any of them).

Renzi’s Jobs Act, passed March 1, ends the system that gave some employees ‘jobs for life’. Companies that hire a previously unemployed worker in 2015 get a three-year grace period on social security contributions. This makes hiring much more worthwhile. As a result, consumer confidence in Italy is now, July 2015, at a 10 year high (the graph does not include the latest few months).

Car sales are up. Youth unemployment is way down. Demand for exports is strong. And debt payments are falling sharply, from the present high level of 5 per cent of GDP to a targeted 1 per cent by 2020.

Renzi’s reforms now enable insurance companies and securitization companies to lend directly to businesses, attracted by a tax break for firms that issue new equity.

Renzi has cut corporate taxes by 6.5 billion euros, and imposed electoral reform for Italy’s lower house. He is trying to slash the amount of pending litigation by half and reduce the length of trials from three years to one.

Renzi is only 40 years old. When appointed, he was 39, making him the youngest Prime Minister in Italy since 1861. His reforms deserve far more attention. (See The Financialist: Italy’s Reform Agenda). Few believed he could fulfill his promises when he took office. But he has. Perhaps France could take a few lessons from Renzi.

Euro Disney Pricing: Pure Mickey Mouse!

By Shlomo Maital

If you’re a manager or entrepreneur, here is a 100% certain proven way to get into hot water. Take the advice of economists. I should know – I am one of them.

EuroDisney is a good example. According to basic microeconomic theory, if you can segment markets with different prices, then you set prices inversely to the price sensitivity (or, elasticity) of demand. Low sensitivity? High price. High sensitivity? Low price.

Many Europeans buy Disney packages on-line. That means that Disney can charge people from different countries, different prices, because the Internet knows where you are. And of course, that’s just what Disney does. Disneyland Paris practices “geo-blocking” (Global New York Times, July 30, p. 18). “For an identical stay, the Euro Disney website often offers higher prices on German computers than on French ones.” Euro Disney had 14 million visitors last year with prepackaged prices. This year? Geo-blocking.

So what’s wrong with price discrimination, if you’re a monopoly and can get away with it? For one, it is not legal. The European Commission says national borders are supposed to be erased, and prices should be the same for all.

But worse than that — discriminatory pricing causes major resentment. Imagine that you bring your family from Berlin to Disney Paris, and find that your neighbor, on the merry-go-round, from Paris, paid half what you did. I know – it happens all the time on airplanes. Nearly everyone on the plane has paid a different price, from very high to very low.

Disney could say: If we charged one price, we’d have fewer customers, and would have to charge EVERYone much more to recover our costs. But this is pure Mickey Mouse!

When economic theory and profit maximization collide with basic fairness and empathy for customers, paying high prices, empathy should win. In the long run, it is simply good business. Beware of what economists advise. It is based on math, not on people.

The New Pricing Model: “Name Your Price. Really!”

By Shlomo Maital

Harvard Business School’s Working Knowledge has an interesting piece by Michael Blanding, about research by marketing assistant professor Shelle M. Santana. Santana studied “pay what you wish” (PWYP) pricing.

PWYP? According to economists, it makes no sense. If you can pay, say, one cent, or nothing, why of course that’s what everybody will do.

Yet another case where economic theory misleads.

“Research shows,” notes Blanding, “that when people are able to set their own prices, almost everyone pays something – and sometimes well over the suggested price.” Santana says she was interested in the broad variance of prices people pay, under PWYP, and who pays a little, and who pays a lot, and when.

She found that by controlling the environment and context, she can influence what buyers are willing to pay.

Some examples of PWYP? Radiohead’s In Rainbows album has ‘name your price’ downloads. Dallas Theater Center has Pay What You Can nights to attract new patrons. Boston Pedicab has an ‘open fare’ system. Panera Bread has four nonprofit Panera locations with PWYP (I wrote a blog about one, some time ago).

In one experiment Santana and a colleague designed a PWYP promotion for a pack of gum at a student café at NYU. At one scenario, their sign showed a pair of hands shaking, and read “It’s Your Turn to Set the Price Today”. At a second, the sign showed a group of hands in a circle, that read: “Because We’re Partners, It’s Your Turn to Set the Price Today.”

Guess which sign got the highest price? Of course – the second sign got an average price of 69 cents, compared with 57 cents for the first. That’s a 21 per cent difference.

Why? Creating a communal norm… pro-group, rather than just pro-self. Moreover, customers are willing to pay more, often much more, when a portion of the proceeds is donated to charity – something many companies discovered long ago.

Harvard Business School Working Knowledge, 22 July 2015. “Research and Ideas”

Internet of Things (IoT): It’s Not Hype

By Shlomo Maital

If you’re like me, you may be skeptical of the term “Internet of Things”. I am so tired of hearing about refrigerators that know how to order milk. This is not a compelling value proposition. But after reading a new McKinsey Global Institute report, I am a lot less skeptical.* Here is a summary.

Definition: “The Internet of Things: sensors and actuators connected by networks to computing systems, to monitor and manage the health and actions of connected objects and machines, including people, animals and the natural world.”

“The Internet of Things has the potential to dramatically improve health outcomes, particularly in the treatment of chronic diseases such as diabetes that now take an enormous human and economic toll…. Technology suppliers are ramping up IoT businesses and creating strategies to help customers design, implement, and operate complex systems – and working to fill the gap between the ability to collect data from the physical world and the capacity to capture and analyze it in a timely way.”

“We estimate that the Internet of Things has a total potential economic impact of $3.9 trillion to $11.1 trillion per year in 2025. (At the top end, the value of IoT impact would be equivalent to 11 per cent of the world economy, or $99.5 trillion in 2025.”)

“By viewing IoT applications through the lens of “settings” we capture a broader set of effects.. a settings lens helps capture all sources of value – we identified nine settings where IoT creates value: Human (devices attached to or inside the body); Home (where people live); Retail environments; Offices; Factories; Worksites; Vehicles; Cities; Outside. “

“ Capturing [the potential of IoT] will require innovation in IoT technologies and business models, and investment in new cpaabilities and talent.”

So: Innovator! Can you think of ways that connecting things digitally brings real value to people? Which of YOUR things would you like to see connected? Start with a setting; proceed to thinking of the sensors you need; and continue by thinking about how you would use the sensors’ data to create value. This is a future industry waiting to be invented.

* McKinsey Global Institute. The Internet of Things: Mapping the value beyond the hype. 2015.

What Goes Up Comes Down: China’s Stock Market Decline

By Shlomo Maital

Between mid-March and early June, less than three months, China’s stock market created $3.5 trillion in new capital gains for its investors. Many of them are working people, who scrimp and save and buy shares. They were richly rewarded.

Between early June and July 7, the Chinese stock market fell by one-third, wiping out $3.5 trillion in capital gains. Over the 12-month period to July 8, the Chinese stock market is still up by 75 per cent!

Once again, for the millionth time, investors learn that whatever goes up, can and will come down. When it does, it often comes down pretty abruptly.

The so-called “crash” in China’s stock market has been greeted with what could be seen as a hasty, panicky intervention by regulatory officials, who suspended trading in over 90 percent of the 2,775 shares listed on Chinese exchanges, as the government tries to quell a sell-off. I still believe that most small investors in China are not selling, are wisely holding on to their shares, and believe, rightly, that they will bounce back.

It all depends on your time perspective. If it is a one-month horizon, well, this is a crash. If it is a one-year horizon, then, Chinese shares are still up by 75 per cent, from July 2014 to July 2015. See the chart below.

With a bit longer perspective, that one-month 33% drop doesn’t seem as steep, does it? And I believe most Chinese investors bought in to the market well before the decline of the past month. If they bought in before March, they are still ahead. That $3.5 trillion in losses is purely paper, purely perception. Why not measure the gains between July ’14 and July ’15?

There is no need for government intervention. The model of Hong Kong (Hong Kong authorities bought shares after the 2008 global collapse, and ended up profiting when share prices rebounded) is not one China Mainland should follow. Sometimes, “do nothing” is the best and wisest policy, in health care and in financial regulation.

Kids’ Scores Rise When They Care About Other Kids & Teachers

By Shlomo Maital

It’s summer vacation time for school kids. A good time to reflect on what they will return to, in September.

In an Israeli weekly, psychiatrist Ron Berger, who specializes in helping children all over the world who suffer from post-trauma stress disorder, recounts an experiment tried at a small school in northern Israel. The school did poorly in national performance tests. Then Berger and colleagues introduced a program, “A call to giving”, which focused on two key elements:

- Mindfulness — “intentional, accepting and non-judgmental focus of one’s attention on the emotions, thoughts and sensations occurring in the present moment”. Simply being aware of one’s own feelings and thoughts in the present.

- Compassion — sympathetic pity and concern for the sufferings or misfortunes of others.

The idea? Create strong bonds among the schoolchildren, first by making each of them aware of their own feelings and identity, then developing a caring attitude toward others, include the teacher.

So – what in the world has this to do with test scores?

Well, apparently a lot. The school now scores among the highest, in Israeli schools, in national tests.

Why? The simple answer could be — kids study best when they like the place in which they go to school, like other kids, like the teachers, and find that the teachers like them. Apparently, children do not thrive in an environment where there is intense pressure to achieve high grades, and where each individual essentially is out for themselves, sink or swim, instead of being part of a tight-knit social community that helps one another.

Is this naïve? Innocent? Simple-minded? Perhaps. But at least at once school, it works. It’s worth a try.

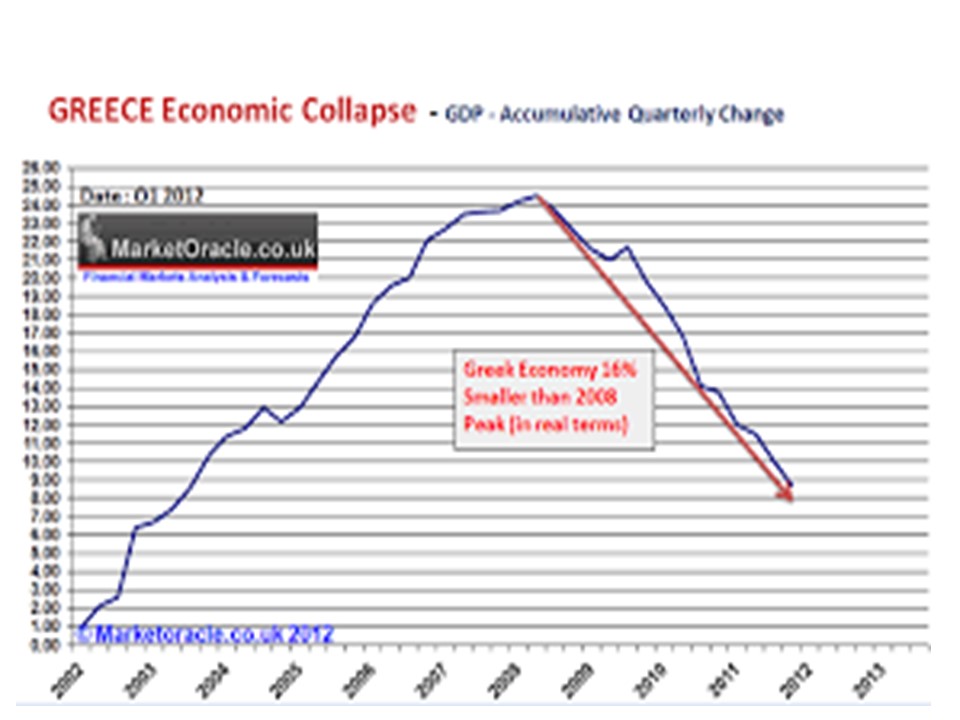

Greece Collapses – Germany and the World Will Pay the Price

By Shlomo Maital

Two trucks speed toward each other on a deserted highway. They are 50 kms. apart. Each drives at 100 kms. an hour. They have 15 minutes before they meet. Plenty of time to slow down, stop, turn off the road.

Yet they still collide head on, with massive damage.

Then, the experts debate why this happened.

This is the story of Greece. Greece joined the EU in 1981. It joined the Euro in 2000, in time to implement paper euros and coins when all of Europe did.

Here is what former European Central Bank Chief Economist Otmar Issing said, in March 2011: “Greece was only able to join the euro through deception [its budget deficit was far above permissible levels] and the currency bloc’s leaders have been “too polite” ever since to deploy adequate sanctions that could have averted the region’s debt crisis. When I worked for the ECB, I suffered every time countries didn’t meet the criteria…Greece cheated to get in, and it’s difficult to know how we should deal with cheaters. … Greece will probably be unable to honor its debts as it grapples with insolvency. The country’s repayment ability remains questionable even after the government endorsed an accelerated asset-sale plan and a package of budget cuts necessary to draw a fifth tranche of its bailout.”

It was obvious in 2011, four years ago, that Greece could not pay back all that it had borrowed. Today its public debt is an unsustainable 177 percent of its GDP. So it is obvious – much of the debt has to be wiped out, one way or another.

Are Greece and its leaders to blame? Sure. But on the principle of “sunk costs”, the history is irrelevant. The question is, what to do today, to avoid the crash? We’ve seen it coming for years, according to Issing. Yet Europe and its blind leaders continued to torture Greece, imposing ever more severe austerity. You cannot grow an economy by shrinking it. And an economy can only pay back debt by growing. Grade 5 kids know that. But politicians and economists don’t. You cannot have a single currency, the euro, without a single united banking system throughout the euro zone with one set of rules. That never happened. It never will. So the euro will become a permanent chronic ongoing crisis, and it has been for years.

Yesterday German Chancellor Angela Merkel said, “if the euro fails, Europe fails.” Really? What has Chancellor Merkel done to recognize reality – Greece cannot, cannot, pay back its debt? She should have said, “The euro has failed, because I have failed, and I therefore tender my resignation. I failed to explain to the German voters, that even if we wipe out a quarter of Greek’s debts, Germany still has gained immensely”.

Who has been the big winner from Greece’s suffering? Germany.

Why? Because Greece has dragged down the external value of the euro, and the cheap euro makes German exports more competitive. If Germany under Merkel would give Greece 3 percent of all it has gained from the Greece-driven euro decline, the crisis would be over.

Some 37 % of Germany’s GDP comprise exports, or nearly $1.5 trillion (in 2014), just slightly behind that of the U.S., whose population is three times bigger. Even China exports only 23 % of its GDP. How strong will German exports be, when Greece leaves the euro, restores the drachma, bankrupts its citizens and its banks, crashes world financial markets, bashes the world economy — and then the euro soars, throwing Germany’s export-driven economy into recession?

Two trucks speeding toward each other for years. Could the crash have bene prevented? Sure, with common sense.

Was it?

No. History will be unforgiving to the hypocritical blind leaders who caused this.

New Thinking About Our Schools: It’s NOT Rocket Science!

By Shlomo Maital

A great many people the world over are troubled about what happens to our children and grandchildren in the school system. America’s No Child Left Behind Act (2000) has left most children behind, because America still scores poorly in international achievement tests, despite (because of?) billions spent on “Race to the Top”.

A simple principle says, if you want to improve, learn from others. Benchmark what others do, adapt it, and get better. But educational bureaucracies in most countries do not even know what global benchmarking is.

Take Finland, for example. Pasi Sahlberg, a Finnish educator, has shared Finland’s experience with the world in his 2011 book Finnish Lessons: What Can the World Learn from Educational Change in Finland? It has been translated into many languages already, including Hebrew.

Here are the four key principles Finland used to create a world-class world-leading educational system, for all Finnish kids, not just a handful of privileged ones in Helsinki.

- Guarantee equal opportunities to good public education for all. In the U.S., that means that schools in rural Louisiana and Mississippi should be up to scratch, as much as ones in Princeton, NJ.

- Strengthen professionalism of, and trust in, teachers. This is related to pay levels, teachers’ colleges, and in general, how society values those who educate our children. In Finland, it’s really hard to get in to teaching programs, as hard as getting in to engineering.

- Get parents involved, educate everyone about education and the key processes, especially assessment (and note: assessment is NOT just tests).

- Facilitate competition and innovation among schools; network them, help them learn quickly from one another, let them try experiments and scale up ones that succeed.

These principles are easy to state, hard to implement. But take #4, for example. President Bush’s very first Act, in 2000, brought free-market competition models to American schools by tying state and federal funding for schools to test performance of kids. Many countries have copied this dumb idea.

There is another way to introduce competitive forces into education. Let schools experiment, and share the results. This is the REAL free-market model. To do this, you need to abandon the insane obsession with testing, hated by kids, parents and teachers alike, and let kids learn to love learning, let teachers love to teach, and evaluate by what children can do, rather than what they can memorize and regurgitate.

In Finland, it worked. How come? What can we learn from it? How many American educators have spent time in Finland, observing their schools, talking to their educators? And how long will it take, before educational professionals all realize that No Child Left Behind left a great many kids behind, far behind, and that it is time to dump the whole bad idea, not only in America but everywhere.

How (and Why) You Should Prepare for a World of Very Slow Economic Growth

By Shlomo Maital

It is becoming more and more clear that in the next 50 years, the world economy (and probably, the economy in which you live and work) will grow more slowly than in the past. What was perceived as a temporary correction, due to the global financial crash of 2008, is now becoming chronic.

Why?

A study by McKinsey Global Research, “Global Growth: Can Productivity Save the Day in an Aging World” (available from McKinsey’s website) notes that “GDP growth was exceptionally brisk over the past 50 years, fueled by rapid growth in the number of workers and in their productivity.” But now, employment growth, which averaged 1.7 per cent yearly between 1964 and 2014, is set to drop to just 0.3 per cent a year.

And productivity growth is slowing too. “Even if productivity were to grow at the (rapid) 1.8 per cent annual rate of the past 50 years, GDP growth would decline by 40 per cent in the next 50 years – slower than the past five years of recovery from recession”. But productivity growth has declined and does not look like it will recover much. China’s economy is slowing. Europe and America grow slowly. Japan has slow growth. Looks like it’s chronic.

What can be done? “Catching up to best practice”, says McKinsey. In other words, if we all benchmarked the world and defined and captured ‘best practice’, productivity growth could nearly make up for the declining growth in workers.

Here are McKinsey’s 10 key “enablers of growth”. Can each of us look at this list closely, and figure out, what is my role? How can I become really skilled, expert, at one or more of these enablers? If McKinsey is right, and if you can, you will be in great demand – and create value for the world.

Here is the list. Which of thee suits you? What must you do, in order to become a true enabler?

- Remove barriers to competition in service sectors. 2. Focus on public and regulated sector efficiency. 3. Invest in physical and digital infrastructure. 4. Foster R&D demand and investment. 5. Exploit data to identify transformational improvement opportunities. 6. Improve eduation and skill matching and labor market flexibility. 7. Open up economies to cross-border economic flows. 8. Boost labor force participation among women, young people, and older people. 9. Harness the power of new actors through digital platforms and open data. 10. Craft regulatory environment, incentivizing productivity and innovation.

by Shlomo Maital

Navinder Singh Sarao

I read this story today in Bloomberg Business, and still just can’t believe it. But it’s true. *

The young man in the photograph is named Navinder Singh Sarao. Today he is in a 10 ft. by 6 ft. cell at Wandsworth Prison, one of Britain’s worst jails.

Why? Five years ago, his actions allegedly contributed to wiping more than $1 trillion in assets off financial markets. Trillion here, trillion there, pretty soon, you have a problem.

Here is the story. Sarao was a graduate trainee at Futex, a company that specializes in trading stocks and other assets. Here is their calling card: “We believe that keeping mind, body and intellect nurtured leads to overall well-being, which is essential for successful trading. Our approach keeps these in balance, and since 1990, when Futex was founded, has helped many traders reach their goals.” Translation? We make money, scads and scads of it, any way we can.

Sarao was an instant sensation. While other traders were eking out 500 pounds a week, Sarao was clearing 500,000 pounds! He always sat by himself. And he spent almost nothing. He was extremely frugal. On a good day, Sarao made $130,000, and even on a bad day, $70,000. He got to keep 90 per cent of the money he made for Futex. But he felt it was not enough. He ended his contract at Futex and went to CFT Financials, a firm that rented out space to private traders. He got backing and technology from MF Global Holdings, the now defunct firm run by former US Senator Jon Corzine that incurred enormous losses for its investors.

“I want to be the biggest trader,” Sarao said.

According to U.S. allegations, Sarao began “a massive effort to manipulate” stock futures on Globes, an electronic trading platform. This involved “spoofing”. It is an illegal technique that involves flooding the market with bogus buy or sell orders to drive prices up or down, then cancelling the orders. Spoofing is rampant today. Sarao built computer algorithms, in June 2009, to change the way his orders would be perceived by other computers. (A very large fraction of trading today, in financial markets, is done by computers, not by humans).

On May 6, 2010, there was a “flash crash”. More than $1 trillion was wiped off the markets in the space of a half hour. Sarao allegedly made $900,000, using an algorithm that gave a misleading impression of the volume of sell orders.

After this crash, suspicion fell on high frequency trading firms – firms that buy and sell assets, using super computers that identify opportunities and act on them in micro-seconds, far faster than humans can. In late April of this year, Scotland Yard knocked on his door in Hounslow, a Western neighborhood of London, and accused Sarao of helping to cause the flash crash.

Yes, a glorified day trader living with his mom and dad near Heathrow Airport nearly destroyed the world. Why don’t you buy a Bugatti? His friends asked. I don’t know how to drive, he answered.

Sarao will soon return to court, in his gray prison tracksuit, and for the 8th time sit in the dock, as the U.S. tries to extradite him on 22 counts, from wire fraud to market manipulation. Sarao denies the charges. Many doubt that he or anyone else singlehandedly caused the flash crash. The truth is, COMPUTERS, not humans, drive markets today. But you can’t put a super computer in jail. Sarao said last May, “I’ve not done anything wrong apart from being good at my job”.

“This guy had balls”, said a Futex trader who knew him. “He used to get into big positions, he saw the risk, he saw the reward, and he took the trades.”

If Sarao is guilty, we should worry about how one person can destroy the market. If he is innocent, we should worry that financial markets are unstable, prone to huge swings and are easy to manipulate, by those who operate in the shadows.

Either way, we are in big trouble.