You are currently browsing the tag archive for the ‘EU’ tag.

The EU is back – the US is not

By Shlomo Maital

The Brexit fiasco generated enormous pessimism about the future of the European Union. There was talk about Italy leaving the EU, after extreme elements there broached the idea, or even Netherlands, which resents handouts to spendthrift EU nations.

Well, the EU is back. Here is what the Financial Times reported on the bailout deal struck yesterday, after four long days of meetings, wrangling and compromise:

“EU leaders have struck a deal on a landmark coronavirus recovery package that will involve the European Commission undertaking massive borrowing on the capital markets for the first time. After days of sometimes bitter debate, the bloc’s heads of government agreed on a €750bn package aimed at funding post-pandemic relief efforts across the EU. The deal was announced in a tweet from Charles Michel, the European Council president at 05.31am (CET) on Tuesday and was hailed by Emmanuel Macron, the French president, as a “historic day for Europe”. The recovery fund centers on a €390bn programme of grants to economically weakened member states — a significantly smaller sum than the €500bn package originally proposed by Berlin and Paris in May. Leaders also signed off on the EU’s next seven-year budget, which will be worth €1.074tn. The deal, orchestrated by Angela Merkel, the German chancellor, and Mr Michel, is the fruit of marathon negotiations under way in Brussels since Friday morning. The summit was the second longest in the bloc’s history, falling just shy of the record set at a meeting in Nice in 2000.”

Once again, Angela Merkel, the lame-duck Chancellor of Germany, long after she announced her retirement, has returned to bring together disparate EU elements – from the autocratic Hungarian leader Viktor Orban, to the frugal four northern nations.

Smaller frugal nations won an agreement to increase their rebates from the EU — Austria’s annual reduction will be doubled to €565m a year ($644 m.) compared with previous proposals, while the Netherlands’ rebate will jump to €1.92bn ($2.2 b.) from €1.57bn ($1.78 b.) .

Contrast the ability of the fraught wrangling 27-nation European Union, moving to help the poor nations among it, with the hopeless helpless United States, where a) President Trump dumped responsibility for battling the pandemic on the 50 state governments and their governors, and saw as a result a horrendous second wave emerge, and b) led Republican opposition to provide financial help to state governments, while pressing them to re-open schools on Sept. 1, without the money it would take to do so safely.

A New York Tmes Op-Ed asks, which major nation will emerge strongest from the pandemic? Not the US. And no, not China. Answer: Germany, the enlightened leader of sanity and compromise in the European Union.

Israel’s COVID-19 Success: Smart? Lucky? Or Just …Young?!

By Shlomo Maital

Israel is deemed to have had relative success in controlling the coronavirus pandemic. It has been counted among the ranks of South Korea, Austria and Taiwan, all of which acted rapidly and effectively, and as a result had relatively favorable statistics.

However, a closer look at the data reveals a different picture.

Source: Meirav Arlosoroff, The Marker, May 28/2020.

A study by Prof. Zvi Eckstein, formerly deputy governor of the Bank of Israel, reaches the following conclusion. Israel and Austria had similar rates of infection — about 1,800 cases of COVID-19 per million inhabitants.

Israel had significantly lower death rates than the EU average (about 1%, compared with 6.3% for the EU), and lower than Austria, (4%). (See Figure above).

However, Eckstein notes, Israel has significantly younger populations that EU nations, and than South Korea and Taiwan, owing to a relatively high fertility rate. In addition, the mortality rate from COVID-19 is particularly high among the elderly, over 65 and over 80. In many countries, most of the elderly are in homes for the aged, which have been notorious incubators for the coronavirus in many countries. In Israel, a relatively larger proportion of the elderly live in their own homes or with children. In Israel, as in the US, there have been tragic cases of infection and death in homes for the elderly, but proportionately fewer such homes limited these tragedies.

So, was Israel smart? Lucky? Or, simply, does it have a younger population, less vulnerable? According to Eckstein, probably the latter. Perhaps this may shorten the very long line of political leaders and officials who would like to take credit.

Surprise: Germany Leads!

By Shlomo Maital

source: IMF

source: IMF

Quiz: Which country in the world is highly conservative fiscally, avoids deficits like the plague (oops, sorry for that one), hassles spendthrift EU nations (like Greece) for excess debt, and in general has acted like Scrooge?

You got it. Germany.

Part two: Which country has seen the extent of the COVID-19 plague clearest and acted most decisively, including massive emergency spending?

Surprise. Germany. Never would have guessed it.

Lame duck Chancellor Angela Merkel, a trained scientist, trained well in the former East Germany, was among the first to predict massive deaths, and drew scorn at the time – but she is proving right, even though Germany, for many reasons, has the lowest relative death toll (relative to the number of cases).

And now, she has led Germany to implement the most extensive, massive emergency bailout plan including huge spending, covering salaries of employers and guaranteeing emergency loans for businesses. No other country comes close. (Alas, my own country is right there at the bottom – though, of course, we do not have as deep pockets as Germany does).

According to the International Monetary Fund, Germany’s bailout package is fully 28% of GDP! And Germany guarantees 90% of emergency loans. All this, to keep businesses afloat, so they can bounce back.

But I have on caveat, or quibble. Germany: all this largesse goes to Germans. How about Italians and Spaniards? Can you spare just a small slice of your luscious pie for fellow EU countries, suffering badly? They’re waiting.

European (Dis)Union: Shame on Them!

By Shlomo Maital

Italy is desperate. With more COVID-19 cases and deaths than China, it is now ‘triaging’ (selecting) those who get medical care and not treating those 60 years old and over. Don’t blame them – they have to, they lack medical equipment and doctors and hospital beds and ventilators.

Wait. Italy is part of the “European Union”, a union of 27 nations banding together to help one another and support one another.

Right?

Apparently, wrong. The nation coming to Italy’s rescue is not the other 26 EU nations, but Russia, which has sent medical supplies and personnel.

(And by the way, United States? Which used to help other nations? Not in the age of Trump… America First!)

Slovakia’s leader noted that his desperate requests for help from the EU were turned down cold. But China did come to the rescue, and it is China which is now sending medical aid to other nations. The press claims it is done to restore China’s image, badly damaged by the fact that COVID-19 originated in China. Maybe, too, it is done because China simply gets it.

European Union? It was not Brexit and Britain that has damaged European union, but the Europeans themselves. Whatever happens in this crisis, Europe will not be the same. If nations in a union do not help one another in time of need, then there is no union.

Shame on you, Europe. I can’t believe that none of the other 26 EU nations can spare any medical supplies or equipment, at all. Nor is there a single EU person in charge of EU overall policy.

It will be very hard for the Europeans to put Humpty together again, after pushing him off the wall and not even offering a bandage.

Understanding the Brexit Disaster:

Ask the Psychologists!

By Shlomo Maital

I’ve been glued to our TV, for weeks, watching the British debate in Parliament what to do next about Brexit. I’ve watched how the world’s oldest elected Parliament cannot find a majority for anything – except, maybe, NOT to crash out of the EU. I’ve watched how the Trump-like PM Boris Johnson tries to circumvent Parliament, in the name of democracy but instead mortally wounding it. I studied for a year in Manchester, and feel deeply sorry for the people of Britain – and am trying to understand how they got into this pickle.

Enter the psychologists. In the excellent podcast Hidden Brain, by Shankar Vedanta, the Harvard University psychologist Daniel Gilbert was recently interviewed. He spoke about this – we humans are incorrigibly bad at predicting the future,, specifically, in predicting how we will feel in future about a decision made in the present.

The British people voted narrowly (52 for, 48 against) to leave the EU, in 2016. Mainly they voted for “take our country back”, a slogan pushed by pro-Brexit politicians, driven by anger at the flood of migrants crossing the English Channel that under EU rules could not be stopped.

But what about other aspects of leaving the EU? What about the Ireland-Northern Ireland border? What about all the EU citizens living in Britain? What about trade, tariffs, customs? Then-PM David Cameron, who initiated the referendum, never believed it would pass, and never developed realistic future scenarios about how leaving the EU would be done. Former PM Theresa May stubbornly pushed the same leave-EU proposal to Parliament three times – despite zero chance of it passing.

Professor Gilbert explains, basically, that when we make a decision, we are pretty hopeless about predicting how we will feel about it. As the Brits learn more about what leaving the EU means – crashing out with no deal, in particular, as Johnson obsessively wants — I believe they regret their initial vote in 2016. In particular — if only 1.5 per cent of those who voted “leave” now change their mind and would vote ‘stay’ – the referendum would be reversed. Yet — cynics, in the name of democracy, say “the result of a referendum is set in stone” – even though Parliament, elected by the people, can change its mind a dozen times a day, also in the name of democracy.

Basically – people are flawed in how they predict how they will feel about a decision in the future. We know this from the work of psychologists, and from our own introspection.

Conclusion: Do another referendum on “leave or stay”. Take into account that humans are flawed. Give the British people another chance.

But Johnson and pro-Brexit politicians insist this is undemocratic. Wrong.

The 2016 referendum was terribly flawed. The British people were not told the full story. They voted on the basis of a narrow idea, ‘take our country back’. They weren’t told, how precisely this would be done.

So – do it again. Offer clear precise scenarios. And offer a clear ‘leave’ plan, including Ireland.

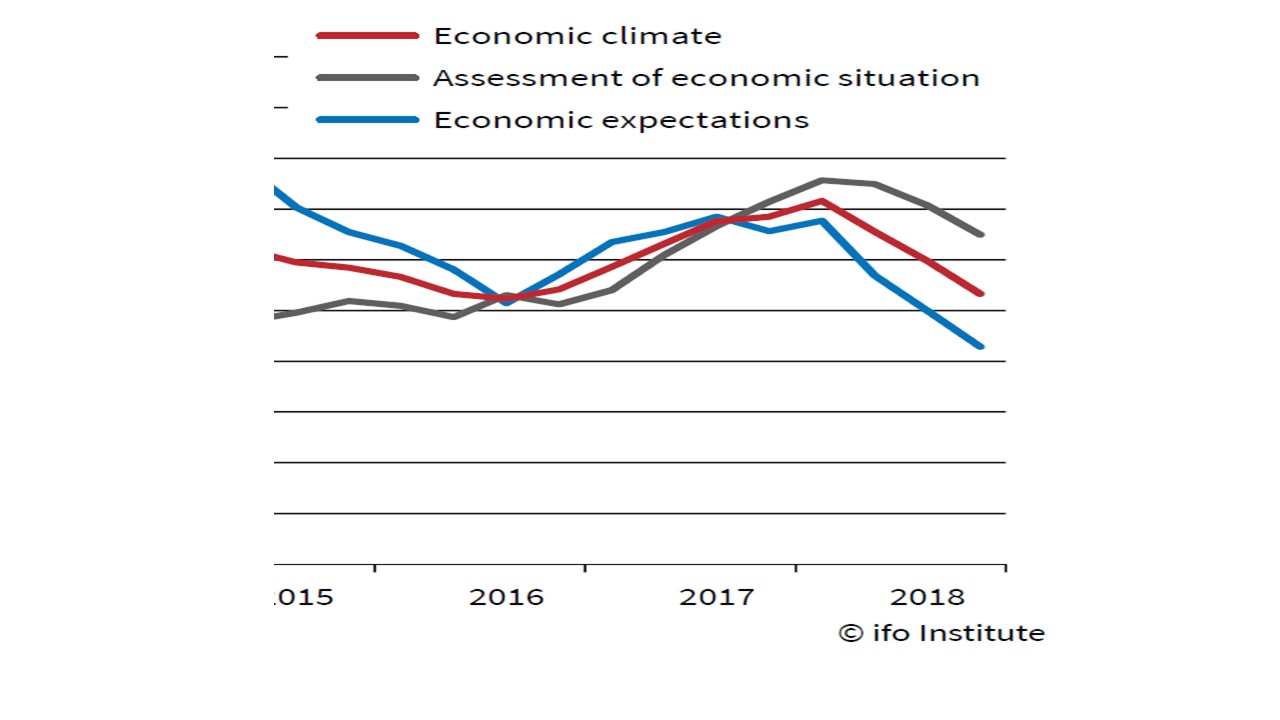

Global Economy: Clouds Gather

By Shlomo Maital

Caption: In the EU, the current state of the economy, and expectations for the near-term future, have both turned down sharply since the beginning of 2018.

I regularly respond to a questionnaire from Ifo – Institute for Economic Research, based in Munich. Ifo regularly surveys economists and business leaders around the world, to put a hand on the pulse of the global economy.

Ifo’s latest report is worrisome. Here are some excerpts from their latest report:

“Sentiment in the euro area continued to weaken this quarter. The ifo Economic Climate for the euro area fell significantly from 19.6 points to 6.6 points, plunging to its lowest level since mid-2016. Experts downwardly revised their assessments of both the current economic situation and their expectations significantly. The euro area’s economy is moving into rough waters.”

There are major problems in Italy and Spain. Italy’s new right-wing government is quarreling with the European Commission. Spain is showing signs of instability. In Germany, Chancellor Angela Merkel announced she will not run again for the leadership of her party, and may possibly resign as Chancellor by year’s end. Hungary is muzzling the press and its judiciary.

The Ifo report continues: “Experts scaled back their export expectations for the euro area, reflecting beliefs that barriers to trade have grown higher. At the same time, a larger number of experts now believe that short and long-term interest rates will rise over the next six months; and that the US dollar will continue to strengthen.”

China’s economic growth is slowing, and the renminbi (yuan) is touching 7 to the dollar. In tomorrow’s election, the US may find itself with a split Congress – Democratic House, Republican Senate. The US stock markets had their worst month in years.

The world is now paying for neglecting countries, and wage-earners, who were left out of global growth and wealth creation. Migration has destabilized Europe, the Mideast and to some extent, the US. If wealth does not come to a country, and if it is not distributed well, many people in that country will flee toward the wealth. And when they do, the resulting instability will put a deep dent in wealthy economies.

Europe’s REAL Problem: Innovation!

By Shlomo Maital

Innovation: Only the Dark Green is “Innovation leader”

The EU has a lot of headaches – more than an ocean-full of Tylenol can assuage. Brexit, and copycat exit movements (including Austria, Catalonia, parts of France, eastern Europe); Greek debts that can neither be paid off nor written off (owing to stubborn German banks); a banking system that has an EU central bank but fragmented country-level banks, that can neither be integrated nor freed and opened; and many more.

Some of these headaches are being (badly) addressed. But one key issue is utterly ignored, as the Washing Post recently noted. * In an EU report, EU Regional Innovation Scoreboard 2016, it is claimed that:

The continent’s most creative and productive regions are in Germany, France, Britain and the Nordic countries. Southern England, northern Denmark, southern Germany and Paris are particularly successful — whereas Romania, Poland and Spain have disproportionately more regions that lack innovation. But as a political and economic union, all of Europe should be worried. Europe is becoming less innovative overall.

Why is this worrisome? One of the main points of a single market is that by creating a huge market, the world’s 2nd biggest economy, you open huge opportunities for entrepreneurs, whose path-breaking ideas can now reach 510 million people (EU), $20 trillion economy (2nd in the world) and per capita GDP of $37,000. But the opposite has occurred. Europe is becoming less innovative, as the report shows.

In Belgium, Greece, Ireland, the Netherlands and Romania, performance declined in all regions,” the report’s authors note. Germany — often considered the economic powerhouse of the continent — was also unable to improve performance.

I taught in France for many years. France has some of the world’s most talented creative engineers. But they don’t start businesses! Why? There are a hundred reasons. Risk, bureaucracy, lack of finance, rigid labor markets…

You can’t solve a problem until you face it. Europe is preoccupied with other problems, and is not even beginning to face its innovation problem. Alas.

* Rick Noack “Where Europe is most and least innovative, in 6 maps,” Washington Post. 2016.

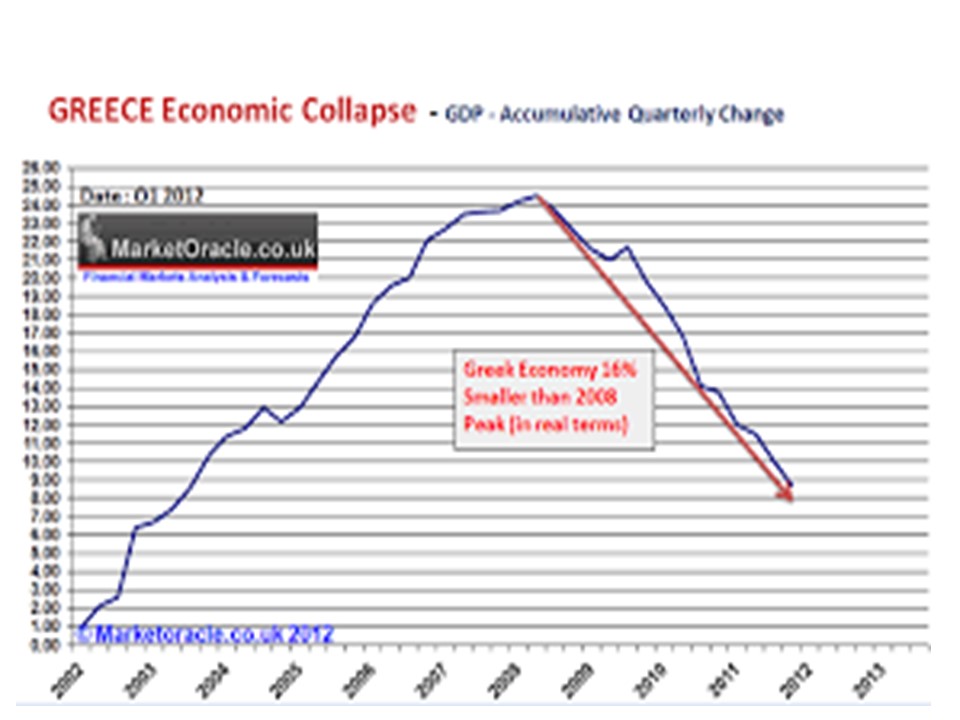

Greece Collapses – Germany and the World Will Pay the Price

By Shlomo Maital

Two trucks speed toward each other on a deserted highway. They are 50 kms. apart. Each drives at 100 kms. an hour. They have 15 minutes before they meet. Plenty of time to slow down, stop, turn off the road.

Yet they still collide head on, with massive damage.

Then, the experts debate why this happened.

This is the story of Greece. Greece joined the EU in 1981. It joined the Euro in 2000, in time to implement paper euros and coins when all of Europe did.

Here is what former European Central Bank Chief Economist Otmar Issing said, in March 2011: “Greece was only able to join the euro through deception [its budget deficit was far above permissible levels] and the currency bloc’s leaders have been “too polite” ever since to deploy adequate sanctions that could have averted the region’s debt crisis. When I worked for the ECB, I suffered every time countries didn’t meet the criteria…Greece cheated to get in, and it’s difficult to know how we should deal with cheaters. … Greece will probably be unable to honor its debts as it grapples with insolvency. The country’s repayment ability remains questionable even after the government endorsed an accelerated asset-sale plan and a package of budget cuts necessary to draw a fifth tranche of its bailout.”

It was obvious in 2011, four years ago, that Greece could not pay back all that it had borrowed. Today its public debt is an unsustainable 177 percent of its GDP. So it is obvious – much of the debt has to be wiped out, one way or another.

Are Greece and its leaders to blame? Sure. But on the principle of “sunk costs”, the history is irrelevant. The question is, what to do today, to avoid the crash? We’ve seen it coming for years, according to Issing. Yet Europe and its blind leaders continued to torture Greece, imposing ever more severe austerity. You cannot grow an economy by shrinking it. And an economy can only pay back debt by growing. Grade 5 kids know that. But politicians and economists don’t. You cannot have a single currency, the euro, without a single united banking system throughout the euro zone with one set of rules. That never happened. It never will. So the euro will become a permanent chronic ongoing crisis, and it has been for years.

Yesterday German Chancellor Angela Merkel said, “if the euro fails, Europe fails.” Really? What has Chancellor Merkel done to recognize reality – Greece cannot, cannot, pay back its debt? She should have said, “The euro has failed, because I have failed, and I therefore tender my resignation. I failed to explain to the German voters, that even if we wipe out a quarter of Greek’s debts, Germany still has gained immensely”.

Who has been the big winner from Greece’s suffering? Germany.

Why? Because Greece has dragged down the external value of the euro, and the cheap euro makes German exports more competitive. If Germany under Merkel would give Greece 3 percent of all it has gained from the Greece-driven euro decline, the crisis would be over.

Some 37 % of Germany’s GDP comprise exports, or nearly $1.5 trillion (in 2014), just slightly behind that of the U.S., whose population is three times bigger. Even China exports only 23 % of its GDP. How strong will German exports be, when Greece leaves the euro, restores the drachma, bankrupts its citizens and its banks, crashes world financial markets, bashes the world economy — and then the euro soars, throwing Germany’s export-driven economy into recession?

Two trucks speeding toward each other for years. Could the crash have bene prevented? Sure, with common sense.

Was it?

No. History will be unforgiving to the hypocritical blind leaders who caused this.

Explaining (again) the Euro/Greece Crisis to Grade 5

By Shlomo Maital

Hello Grade 5’ers! Thanks for inviting me. I know my subject, money and economics, is BOOOOOring. But believe me, it is important for you to know what is going on, because when you are just a few years older, what happens in Europe will affect you. Because Europe is the world’s biggest, or next-to-biggest, economy, depending on how you add the numbers.

So here’s the deal. Europe has had lots and lots of terrible wars, with France, Germany England and others fighting each other. Someone (in France) had a great idea. What if we stopped fighting and made money together, by buying each other’s stuff? If you buy my stuff, I’m not likely to want to fight you. So they called it the European Single Market. And it worked beautifully. No-one thinks Europe will have a big fight any time soon (though, Russia may be an exception – that’s another scary story).

If you sell and buy, you use money. But there are 28 countries that belong to this European club. What a mess if you have to start finding escudos, guilders, lira, pounds, francs, and all kinds of weird money. So 19 of the countries decided they would use the same new currency, which they called the “euro”. Kind of like America, where the 50 states all use the same money, the dollar. Some 332 million Europeans use the euro.

But there is a problem. If you have the same money, you have to have the same rules for making the money. That means, you have to get all those 19 countries to agree on the “rules of the game”. You can’t play baseball or football if neither team agrees what the rules are, right? And here is where things broke down.

Some countries want there to be lots and lots and lots of euros. Some countries want just a little bit of money. Some countries (like, a little country called Greece, only 11 million people) broke the rules, spent too much money, and got into trouble, just like we do when we spend too much. Because they had to borrow and now they have trouble paying back what they owe. Other countries, like Germany, who had lots of money, helped Greece but sent Greece kind of to the penalty box. No more spending. Less treats, less goodies. And Greece didn’t like it. I wouldn’t either.

So Greece has had elections and its new leaders are making a big fuss about the punishments other countries have given it. Some think Greece might even leave the ‘club’ (the euro). That might be terrible, because then some other countries might do the same, and the whole club would collapse. So, the 27 countries want Greece to stay in the club but they do not agree how to make that happen. It’s like, do you punish the Greek people for overspending (they didn’t do it, their leaders did)? Do you forgive them, and then others might do the same? Why should other countries give money to Greece? But if they don’t, they will lose too, because the whole Euro club might come apart.

And you know, Grade 5’ers, I guess you could see this coming. If you start a game, and you have not all agreed clearly on the rules, including for things that are really strange (like, what if two guys are on second base – who’s out? What if one player’s mother comes on the ice and drags him (the goalie) off to Hebrew School? (yup, happened to me) – you’re going to get into trouble. Those Europeans, they started a club without a clear set of rules, and worse, without any way of leaving it without causing REAL trouble.

I’m pretty sure they will muddle through and keep that weird euro club going. They all have too much to lose. But boy, kids, I think you Grade 5’ers could have done a far better job. Those Europeans, they couldn’t see their fingers even if they were right in front of their nose. So, when you go to play a game, or start a club, make sure everyone knows the rules. Kids usually do. It’s the grownups who are dumb about that sometime.

A Deep Contrite Apology to the people of Greece

By Shlomo Maital

Greece’s new prime minister Alexis Tsipras has been sworn in and vows to lead an anti-austerity coalition. He could possibly lead Greece out of the euro and back to the drachma. This would be unspeakably painful for Greece, in the short run, but possibly best in the long run.

Meanwhile, we economists all owe Greece an apology. We have caused immense suffering, needlessly, to 11 million innocent Greeks. According to Nobel Laureate Paul Krugman, economists drafted the ‘troika’ agreement in May 2010, under which the IMF, European Central Bank and European Commission lent Greece money, in return for extreme austerity. Greece had no choice in the matter.

This document assumed Greece would suffer only a small contraction in 2011 and by 2012 would be recovering. Yes, unemployment would rise to 15 per cent (Would Merkel’s Germany ever accept such a scenario??) in 2012, but then it would fall rapidly. Why? Because austerity would work quickly, heal Greece’s economy, and restore growth.

Really? Did the troika economists ever find a single (just one! One!) example in history where austerity worked?

No. There are none.

Instead, Greece suffered a depression, 28 per cent unemployment, its young people migrated abroad, learning German for instance, and youth unemployment reached nearly 60 per cent.

Greece kept its part of the bargain, slashing public spending by 20 per cent. But the promised benefits of austerity turned out to be disaster. That is why Tsipras won the election. And it is why the euro has dived. The EU and its economists brought it on themselves.

It isn’t complicated at all. To heal a budget deficit, you need a growing economy, because when the GDP grows, tax revenues grow much faster, 1.5 times faster. To get a growing economy, you need spending and demand. If people can’t spend, because they have no jobs and their wages are falling, only the government can take up the slack. But if you slash government budgets, the economy will shrink, not grow, and the debt problem will become even worse. That is what ‘austerity’ does. It’s pretty simple.

On behalf of my fellow economists, I would like to apologize to the people of Greece. We screwed up. And worse of all — none of those responsible seem willing to admit it.